We may receive a commission if you sign up or purchase through links on this page. Here's more information.

If you’ve been having difficulty getting the savings habit in gear, there’s help on the way. Digit is an app you can connect to your bank account, that will analyze your spending and automatically move small amounts of money from your checking account into a Digit savings account.

By tracking your spending patterns, the app can predict how much extra you’ll have available in your checking account to move into spending. Through a succession of small transfers to savings, you’ll move from being a non-saver to a regular saver in a matter of days, and with no extra effort on your part.

Interested? Read on…

Table of Contents

What is Digit?

Digit is a micro-savings app launched in 2014, and available for iOS and Android mobile devices. The app is free to download, and connects directly to your checking account. By analyzing your deposits and spending patterns, the app is designed to transfer small amounts of money into a dedicated Digit savings account. The company claims the app as enabled participants to save more than $1 billion since it began.

By making transfers – when extra funds are available in your checking account – of anywhere between $5 and $50 each, it enables you to build up savings, even if you’ve never been able to save money in the past.

Next to the capability of the app to enable you to save money, the most outstanding feature is that the savings activity largely happens out of sight. You go about your regular spending activity, and Digit works behind the scenes to do the hard work of saving money for you. It enables you to passively accumulate savings, while you go about your ordinary business.

How Digit Works

You start the process by connecting the Digit app to your checking account. Once connected, the Digit algorithm analyzes your account balance, pattern of income receipts, upcoming bills, and recent spending. Through that analysis, the app will determine small amounts of extra money available in your account. As it does, those funds will be automatically transferred into your Digit Savings Account.

The small savings transfers are referred to as “debits” (reductions in your checking account balance). But you don’t have to rely exclusively on debits to build your savings. You can choose to manually add money to your Digit Savings Account at any time.

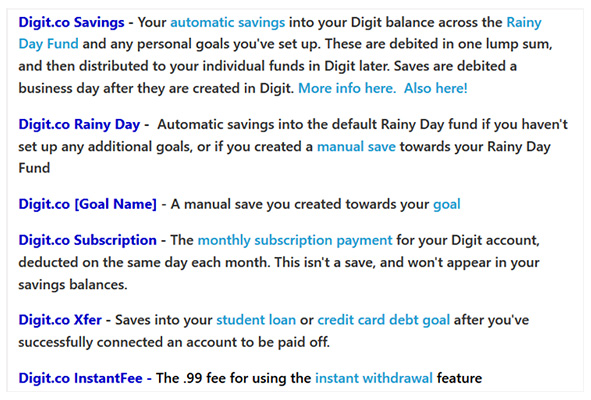

When a debit is charged to your account, you’ll receive one of the following six codes to indicate the purpose of the withdrawal:

As you can see from the screenshot above, you’ll have the option as to what specific goals your Digit savings are targeted for. The Rainy Day Fund helps you to save money toward an emergency fund. Alternatively, the saved money can also be transferred to pay a debt, like a student loan or credit card. Or you can simply set a savings goal, and make manual transfers to build up the balance.

In that way, not only does Digit allow you to save money, but also to do it for very specific goals. The ability to have debits transferred directly into linked loan accounts can enable you to accelerate the payoff of outstanding debts.

The funds in your Digit Savings Account are held in a third-party FDIC insured bank. You won’t earn interest on the account, but instead it pays a savings bonus of 1% on an annualized basis.

Monthly statements are available to download by PDF versions.

Boost feature. This feature enables you to increase the amount the app sets aside toward a specific goal. It doesn’t find extra savings in your account, but rather emphasizes one savings goal over another.

Additions and withdrawals. In addition to debits from your checking account to either savings or that pay down, you can also make manual savings additions. The transfers can be made directly from the app, moving funds from your checking account to savings or debt payoff.

You can also withdraw funds from savings back into your checking account right through the app.

Digit Features and Benefits

Where your Digit savings are held: Digit is an app that connects to your checking account. It is not a bank. When funds are transferred from your personal bank checking account into your Digit Savings Account, they are held in an FDIC insured third-party bank.

Digit app availability: Digit is currently available only for US-based banks, but is also offering a wait list for residents of Canada and the United Kingdom.

Earning interest on your savings: Your Digit savings account is not interest-bearing. Instead, you’ll receive a 1% annualized savings bonus, payable every three months. The savings bonus is more than 10 times higher than the average bank savings account interest rate of 0.09%.

Overdraft protection: If you incur overdraft fees from your bank for excessive withdrawals by the Digit app, you’ll be reimbursed for up to two incidents per year. Though Digit promises overdrafts will be a rare event.

Mobile app: Digit is available at the App Store for iOS devices, 9.0 and later, as well as watchOS 3.0 and later. It’s compatible with iPhone, iPad, and iPod touch. It’s also available on Google Play for Android devices, 4.1 and up. The app gets a rating of 4.7 out of five at the App Store, and 4.3 out of five at Google Play.

Customer service: Contact is limited to email and text messaging, though they do offer answers to most of your questions through their comprehensive Help Center. Regular business hours are Monday through Friday, from 9:00 am to 5:00 pm, Pacific time, and they strive to provide responses to all inquiries in under 48 hours. However, there is no direct phone contact available.

Digit security: Digit uses state-of-the-art security measures that make your personal information anonymous, encrypted, and securely stored. Meanwhile, funds held in your Digit Savings Account are FDIC insured, for balances up to $250,000.

Digit fees: Digit has a single fee structure, which is $5 per month, and you can cancel the service at any time. While that will certainly add an additional cost to your monthly budget, the savings it will generate – particularly if you’ve never been a saver in the past – will make it a small price to pay.

Referral fee program: Refer a friend or family member to the Digit app, and you’ll earn $5 for each referral, which will be moved into your savings account. You can do this by using an assigned referral link to anyone you refer to the app.

How to Sign Up with Digit

To be eligible to sign up with Digit, you must be at least 18 years old and have a US-based bank checking account. At the present time, you can connect the app only to one checking account. Though the company is considering adding capability of additional checking accounts in the future.

To sign up for the service, you’ll need to enter your mobile phone number, then create a password. You’ll then need to enter your checking account information so that the Digit app can connect with it.

Digit can automatically connect to thousands of financial institutions, including banks and credit unions. However, it may take the app several days to complete the connection to your bank account.

Digit Pros & Cons

Pros:

- Digit automates the savings process, enabling you to build up savings without any additional effort on your part.

- You can add a secondary user to your account, though that person won’t be able to access the administrative dashboard.

- You can earn a bonus of 1% on your accumulated savings balance, which is much higher than the interest paid on typical bank savings accounts.

- The app can convert you from a non-saver to a saver without requiring you to change your behavior.

- Digit pays a $5 referral bonus for each friend or family member you refer to the service.

- Your Digit savings account funds are fully FDIC insured for up to $250,000.

Cons:

- You can connect the app to only one checking account.

- Digit does not support PayPal, Green Dot or NetSpend accounts.

- The app connects only with US-based banks.

- The $5 monthly fee does somewhat eat into your potential savings.

- Digit does not offer phone contact.

Should You Sign Up with Digit?

If you’ve been unable to get into the habit of saving money on a regular basis, you’re hardly alone. Many millions of people are in the same boat. But if you want to change that pattern, and become a confirmed saver, Digit is the kind of app that will help you get there. Simply by linking the app to your checking account, Digit will begin finding extra money in your account, and moving it into savings. No additional effort will be required on your part.

The savings account you’ll be moving your funds into won’t be interest-bearing. But it will pay an annual 1% savings bonus, and that’s higher than the interest you’ll be paid at the vast majority of banks. And for safety, the funds in your savings account are held at an FDIC insured bank.

But apart from saving money, you can also use Digit to help you get out of debt. You can do this by setting paying off a credit card or a student loan as one of your goals. Digit will automatically move extra funds toward the payoff of those loans. Very similar to accumulating savings, the paydown will be automatic, requiring no additional effort on your part.

Digit does charge a monthly fee of $5, but that’s a small price to pay to move yourself from non-saver to saver, as well as to get out of debt faster. The best part of all is that once you sign up for the app, there’s nothing more you need to do. But if you want to accelerate the savings or debt payoff process, you can take advantage of the Boost feature, that will emphasize a specific goal in the debit process, enabling you to reach the goal faster.

If you’d like more information, or you’d like to sign up for the app, visit the Digit website.

Author:

Kevin Mercadante is a freelance personal finance blogger and the owner of his own personal finance blog, Out of Your Rut. A recent transplant to New England, he has backgrounds in both accounting and the mortgage industry.