Can I Withdraw My Contributions From a Roth IRA Without a Penalty?

Personal TaxesYes, you can withdraw your contributions from a Roth IRA without penalty (or taxes) — even if you aren’t age fifty-nine-and-one half and even if you haven’t had your Roth IRA for at least five years!

Treasury Regulations § 1.408A-6 says:

“A distribution from a Roth IRA is not includible in the owner’s gross income if it is a qualified distribution or to the extent that it is a return of the owner’s contributions to the Roth IRA.”

In even plainer English, IRS Publication 590-B says in the Roth IRA “Are Distributions Taxable?” section:

“You don’t include in your gross income qualified distributions or distributions that are a return of your regular contributions from your Roth IRA(s).”

And this isn’t some arbitrary rule; it makes complete sense if you think about it.

You’ve already been taxed on the money you put into your Roth IRA; this means that you have basis in your Roth IRA (and this basis should be reported on Form 8606, Line 22).

You shouldn’t be taxed again when taking out the amount you put in.

Table of Contents

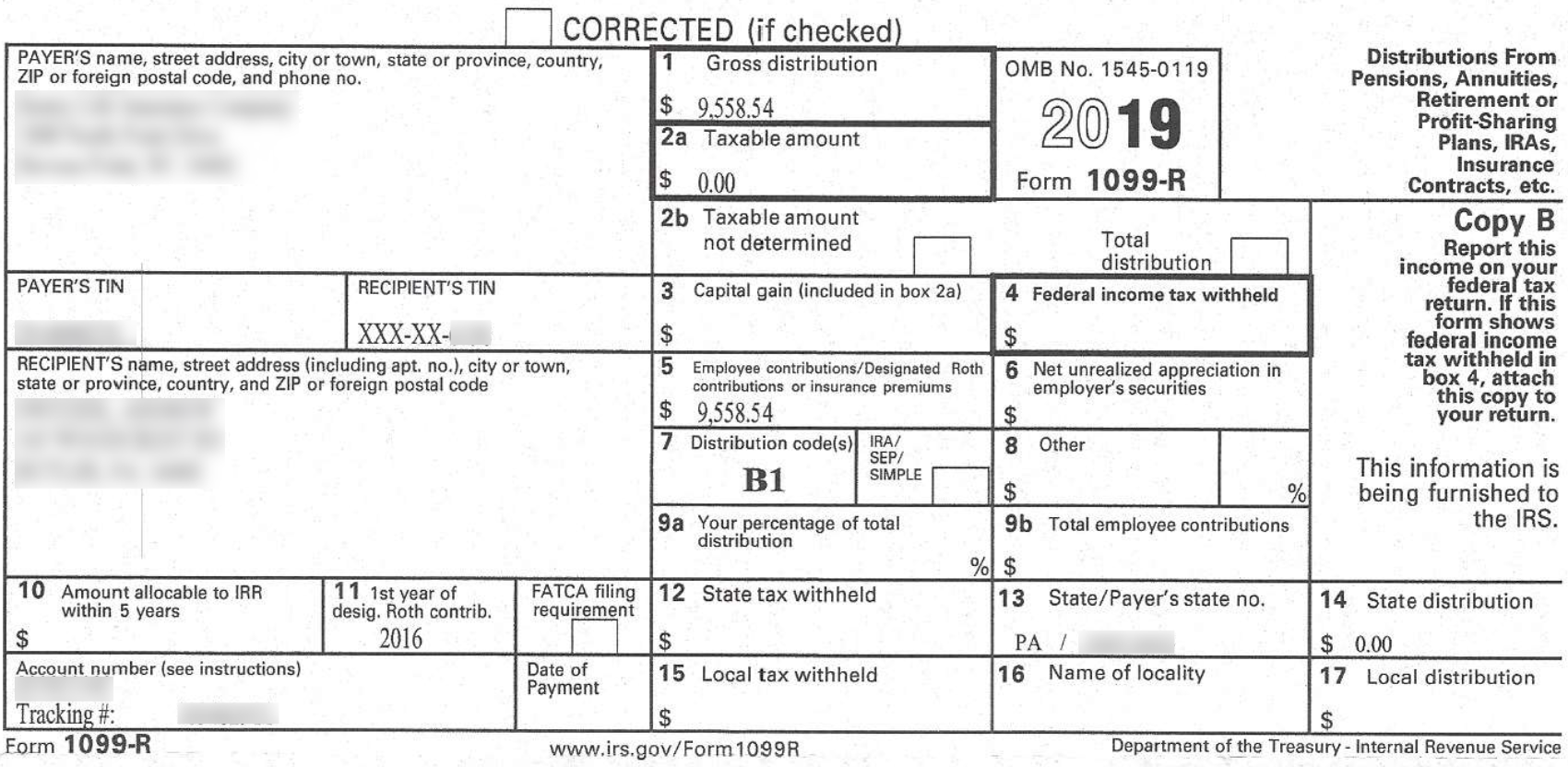

Roth IRA Contribution Withdrawal Form 1099-R Example

Here’s the redacted version of an actual Form 1099-R that one of my clients received.

You’ll see that his gross distributions in Box 1 were $9,558.54 — and that this exact amount was found in Box 5.

This indicates that this entire distribution from his Roth account was tax-free because it was completely made up of withdrawals of contributions.

Withdraw Contributions From a Roth IRA Example

To make this crystal clear, let’s walk through an example.

Let’s say you taxpayer make $50,000 this year in W-2 income, and of that $50,000, you put $6,000 into a Roth IRA.

You’ve already paid tax on that entire $50,000, and you obviously didn’t get any tax benefit for putting $6,000 into the Roth IRA (because it’s a Roth).

And let’s say you forgot to invest the money in the Roth IRA, so it’s just sitting in cash, earning no interest.

Let’s say that next year you make absolutely no money and withdraw the $6,000 in the Roth.

You shouldn’t be taxed on that $6,000, given that you were already taxed on the $50,000 from which the $6,000 contribution was derived.

Roth IRA Contribution Withdrawal FAQs

Here are some common questions that you may have about withdrawing your Roth IRA contributions.

How are returns of contributions to a Roth IRA reported on my tax return?

You report the amount of your distribution on Form 8606, Line 19, and you report your basis in your Roth IRA on Form 8606, Line 22.

Does the five-year rule apply to withdrawals of contributions from a Roth IRA?

No, the five-year rule does not apply to withdrawals of contributions from a Roth IRA.

How do I determine how much of my Roth IRA withdrawal is a withdrawal of my contributions and how much is a withdrawal of my earnings?

According to the ordering rules found in Treasury Regulations § 1.408A-6, any amount distributed from your Roth IRA is treated as being first made from your contributions and then from your earnings.

So let’s say that you’ve cumulatively contributed $20,000 to your Roth IRA. The first $20,000 in distributions from your Roth IRA are therefore treated as returns of contributions — tax-free and penalty-free!

Any distributions beyond this amount would be treated as a distribution of earnings, subject to income tax and the 10% penalty assuming the distribution is not a qualified distribution.

Won’t people just use a Roth IRA as a temporary savings account rather than a true “retirement” account?

Yes, some people will. There are plenty of articles online — like this one — about using one’s Roth IRA as a savings account / emergency fund.

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.