We may receive a commission if you sign up or purchase through links on this page. Here's more information.

Today, I’m discussing how dividends are taxed. As you know if you’ve taken my course, I’m not a huge proponent of dividend stocks. Nevertheless, whether you’re an intentional dividend investor or not, you almost inevitably own at least one security that pays dividends that need to be reported on your tax return.

Table of Contents

Form 1099-Dividend

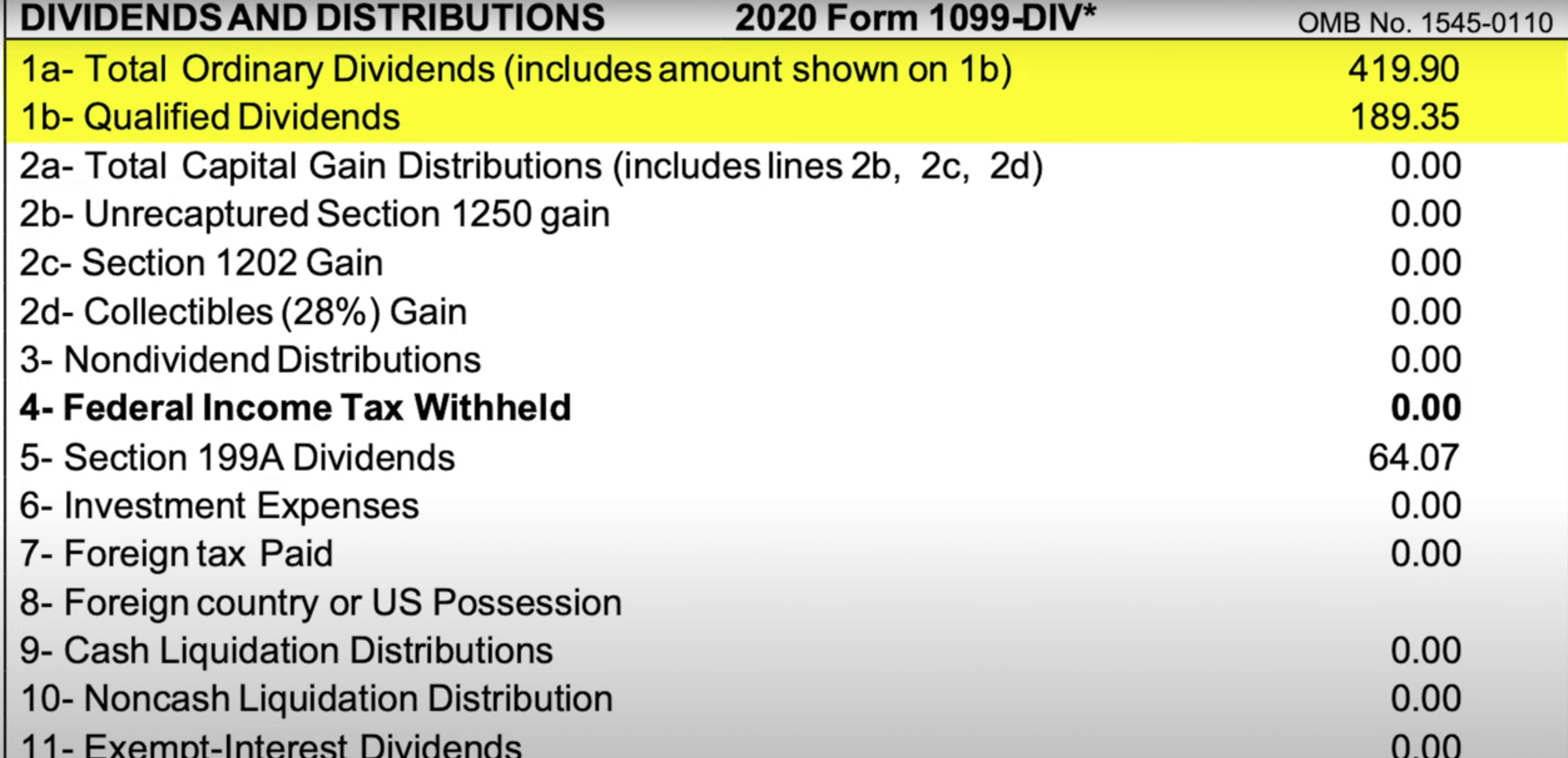

If you earned $10 or more in dividends from a single brokerage last year, you likely received a Form 1099-Dividend in the shape of a PDF containing a Form 1099-B and your gain/loss statements for the year. Last year, for example, M1 Finance, a brokerage I use to invest in small-cap and mid-cap stocks, sent me this Form 1099-Dividend.

For the purpose of this discussion, I’m largely going to focus on lines 1a and 1b. Line 1a lists your total dividend earnings over the year, while Line 1b lists your total qualified dividend earnings over the year.

Check out my video on how dividends are taxed:

Qualified vs. Non-Qualified Dividends

Qualified dividends are usually dividends received from a U.S. company on a stock that you’ve held for at least 60 days. Instead of being taxed at normal income tax rates like non-qualified dividends, though, qualified dividends are taxed at long-term capital gains rates.

Imagine you buy 1,000 shares of X Company in January and then receive $1,000 in dividends a month later. You then sell 200 shares of X Company and hold the remaining shares for the rest of the year.

In this case, 80% of your dividend income, or $800, would be qualified since you held it for at least 60 days, while 20%, or $200, would be non-qualified since you sold it before 60 days. Thus, your 1099-Dividend would show $1,000 in Line 1a, total dividends, and $800 in Line 1b, qualified dividends.

Obviously, if you earned your dividends in a tax-advantaged account like a 401(k), IRA, or HSA, you can enjoy tax-deferred or tax-free growth without the need to report these dividends on your tax return. However, if you received your dividends in a normal taxable brokerage account, you do need to report them on your tax return.

Your non-qualified dividends will be taxed at your normal income tax rates. For example, if you fall into the 12% tax bracket, you’ll pay 12% tax on your non-qualified dividends- in our example, $24 on your $200 of non-qualified dividends.

On the other hand, qualified dividends qualify for the same tax rates as long-term capital gains.

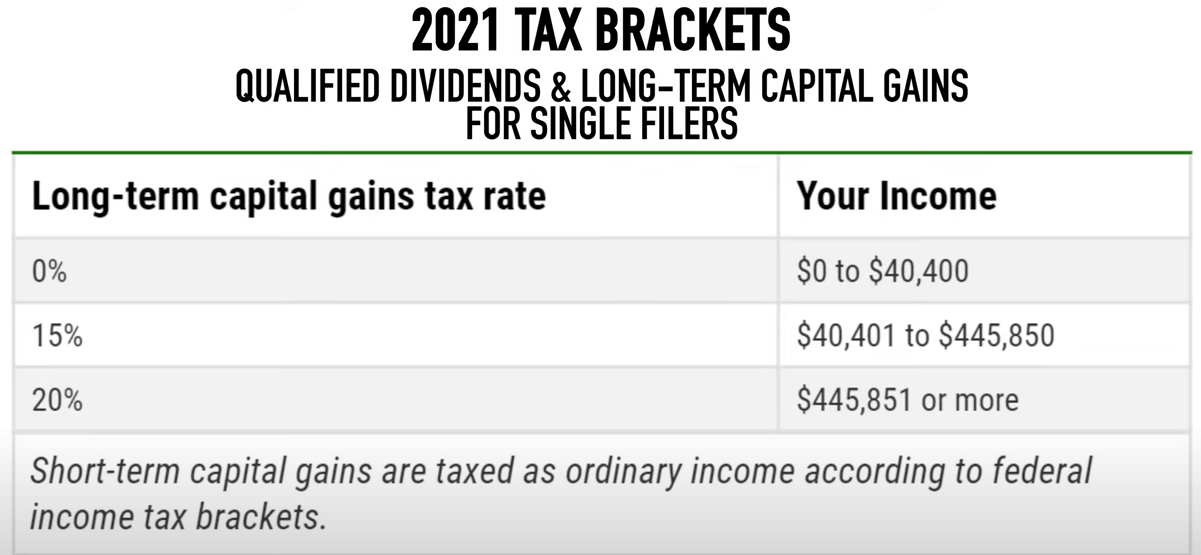

As you can see here, if you’re single and have a taxable income- your whole income minus your standard or itemized deductions- of $40,400 or less, you have a 0% tax rate on your long-term capital gains and qualified dividends, meaning that in our example, you would pay no federal tax on your $800 in qualified dividends.

For single taxpayers with taxable incomes between $40,400 and $445,850, the tax rate for qualified dividends is 15%, while the rate is 20% for single taxpayers with incomes above $445,850. To see the rates for other filing statuses, you can check out this link here.

Schedule B

If your combined dividend and taxable interest amount exceeds $1,500 a year, you’re required to file a Schedule B along with your tax return, which is usually done for you by your tax software (you can check out my TurboTax review here).

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.