-

Upstart

Upstart- Best For: Those who prefer a lending platform that takes into account a variety of factors in addition to credit score, such as education and employment.

- Pros: Upstart takes a more holistic view of a borrower’s background and qualifications than many other lending platforms.

- Cons: You’ll likely need at least a 620 credit score, and you can only choose between a 3-year and 5-year term.

- APR

Typically 6.46 – 35.99%

- MINIMUM CREDIT

620

- TERMS

36 – 60 Months

- ORGANIZATION FEE

Zero – 8%

We may receive a commission if you sign up or purchase through links on this page. Here's more information.

When you’re searching for unsecured personal loan options, one name you’ll come across is Upstart. We’ll take a deep dive into this lending platform so you can decide if it might be a contender for your situation.

Table of Contents

Upstart Overview

Here’s an overview of the Upstart personal loan platform.

What Is Upstart?

An online lending platform, Upstart teams ups with banks, matching clients with a lender, so they can land personal loans ranging from $1,000 to $50,000. These funds can be used for a variety of things such as paying off credit card debt, pursuing debt consolidation, or retiring medical expenses.

The company opened in 2012, at that point offering income share agreements. It moved toward the personal loan sector in 2014.

Upstart Personal Loan Highlights

Upstart’s loans are unsecured, which means you don’t have to put up collateral to get one. That can be attractive for borrowers who need a loan but don’t own a car or house to help secure one.

With some personal loans, the lender only looks at a couple of key facts, such as income and credit score, before making a decision.

Upstart uses artificial intelligence to take a closer look at the complete picture of each applicant. They consider many factors before making a decision.

While they still look at credit score and income, they also consider education level, grade point average while in school, employment history, and even college major.

Upstart Personal Loan Details

As the old saying goes, the devil is in the details. In money matters, that saying often proves true.

Let’s take a look at the loan details for Upstart so you can compare them to the other companies you’re considering.

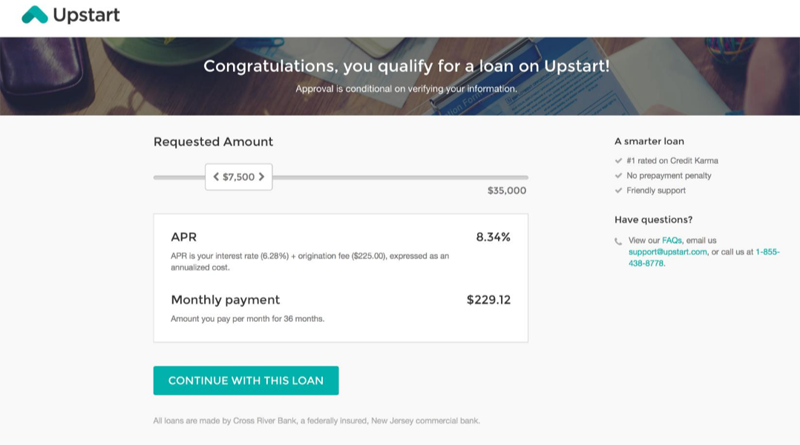

APR

Upstart’s typical APRs range from 6.46% to 35.99%. This range is so broad because Upstart is not in itself a lender; it is a lending platform that matches borrowers with lenders.

However, if you qualify for the lower end of the range, that’s a pretty competitive APR for a personal loan. But if you qualify for the higher end, you may want to look at other options.

While it’s still a better choice than a payday loan, there might be cheaper alternatives for you. For instance, SoFi, another personal loan provider, offers APRs ranging from 5.99 – 21.08% for loans in the amount of $5,000 to $100,000.

The underwriting decision is made by taking a look at the individual’s education and employment history, as well as other factors. But the higher your income, the better your credit history, and the higher your level of education, the more attractive your offered APR will generally be.

If you don’t earn much over the lowest threshold allowed, you haven’t completed much schooling, and you are near the 620 credit score cutoff, you can expect an APR toward the higher end of the range.

Fees

While Upstart doesn’t have any prepayment penalties in case you want to pay off your loan early.

It charges origination fees, which are fees charged for the cost of processing a loan, of zero to 8 percent. If you decide to apply for a loan with Upstart, remember that the origination fee will be taken off of the loan amount before it is transferred to your account.

It’s important to know that so you can factor that into your calculation of how much money you need to borrow.

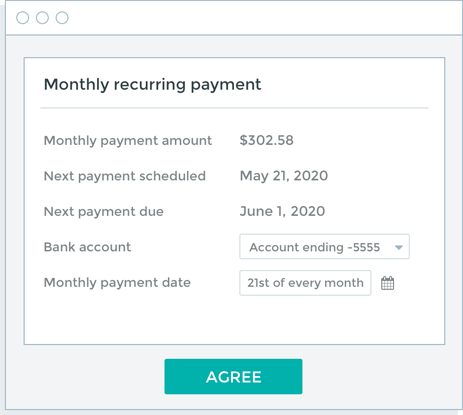

In addition, with Upstart, late fees can be charged when the borrower is 10 days or more late with a payment. The fee is whichever is higher — $15 or 5 percent of the past due amount.

Taking advantage of their automatic pay feature can help you avoid late fees.

Those who have insufficient funds for an authorized bank transfer or who have a check returned to them because of a lack of funds will be charged a fee of $15 each time.

To receive paper copies of your records, you’ll pay a one-time fee of $10.

| Amount | 0% – 8% of the target amount | The greater of 5% of monthly past due amount or $15 | ||

| Frequency | One time | Per occurrence | Per occurrence | Upon request |

Transparency

Upstart’s name and contact information are clearly listed on its website. The APR range is listed in a prominent location on the website, as is the fact there is no prepayment penalty.

But it’s harder to find the information about the fees Upstart does charge. They don’t make that as obvious.

It is available if you do a little digging on their site, however. It can be just as hard, or even harder, to find that information on some competitors’ websites though.

Flexibility

Upstart only offers a 3-year or 5-year term, which isn’t as wide of a range as some other lending platforms. The company also doesn’t offer deferments for lenders who are struggling to repay their loans. There is little recourse for borrowers who need to renegotiate their terms.

They aren’t the most flexible company to do business with, although they do give you a 10-day grace period on late payments before they charge a fee.

Funding Speed

You can have your money as fast as one day after accepting your loan. But those who are using the money for education-related expenses will have to wait three business days before receiving funds.

That’s not Upstart’s fault, though — it’s a federal law.

Overall, they are very quick when it comes to processing loans and issuing funds.

Accessibility

Here are the requirements to get a loan:

- A credit score of at least 620, if you have a credit score.

- You must make at least $12,000 per year through a job, disability or retirement income, or have a verifiable job offer.

- You must also have no bankruptcies or delinquent accounts.

- You must live in the U.S. Upstart is available in all 50 states except for West Virginia and Iowa.

- You must be at least 18 years old, or at least 19 if you live in Alabama or Nebraska.

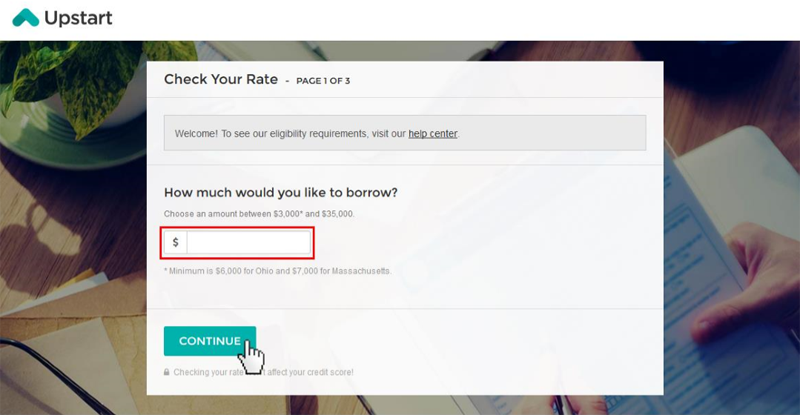

How to Apply for an Upstart Personal Loan

Interested in applying for an Upstart loan? The process is quick, easy, and is all done online. Here is what you’ll have to do.

Step 1: Fill Out the Form

Fill out the online form. It will take about five minutes. You’ll be asked a range of questions such as:

- How much you hope to borrow.

- What your highest level of education is.

- What your primary source of income is.

- How much you have saved up in checking, savings, and investment accounts.

- If you’ve taken out any new loans within the last three months.

Step 2: Review Loan Terms

If approved, you’ll look over the terms of your loan and either accept it or deny it. As with any loan offer, you should carefully read the terms and conditions to make sure there are no surprises.

Step 3: Receive the Funds

Receive the funds, and start paying your monthly payment. Make sure to pay on time each month to avoid fees and so you can improve your credit score.

Upstart Consumer Reviews

One way to rate a company is to look at consumer reviews. But you have to be careful when deciding how much weight to give reviews.

For every bad review, there are likely many other customers who were happy with their service. People are more apt to leave reviews when they are unhappy than when they were satisfied.

So, pay attention to reviews, but do so with a discerning eye.

Better Business Bureau

Upstart has been a BBB accredited business since 2015, and it boasts an A+ rating.

Of the 33 reviews on the BBB site, Upstart received an average of just under 3 stars out of 5.

Upstart publicly responded to many of these reviews, including one review in which an applicant was allegedly treated rudely by an Upstart employee. Upstart responded that it was an isolated incident and the employee was terminated.

Some of the negative reviews were from people who didn’t understand the Upstart process — they thought they were being asked their education level as a scam. They didn’t know that was one of the criteria Upstart uses for determining loan approvals.

Some of the positive reviews highlighted how quick and easy the process was, as well as how quickly the money was received.

User Reviews

On TrustPilot, there are almost 6,000 reviews of Upstart. Of those, 96 percent rated Upstart as excellent, 3 percent rated them as great, and 1 percent rated them as bad.

One reviewer, Monica, had this to say about her poor experience: “I applied for a loan and after almost a week of waiting, they sent me an email that I am approved…They did a soft pull last week on my credit so I proceeded. And then they declined my application.”

Another poor review came from Rudy, a reviewer who claimed to have a high credit score. They had this to say, “I wanted to get a loan for a 1000.00 dollars and with a credit score of 790 and u want to charge me 28 percent interest.”

Another customer, Amanda, who rated it four out of five stars, said she was happy with Upstart. “I got a great rate, and quickly.

The email notifications were confusing and seemed a bit out of order, but all worked out.”

A client, Shannon, who gave Upstart a 5-star review had this to say: “This is the only way I will ever take out a personal loan. I used Upstart to consolidate high interest credit cards.

The process is simple, expedient and user friendly. Funding happens lightning fast.”

Upstart Pros and Cons

As with any other company, there are pros and cons of doing business with Upstart.

Upstart Pros

- Unique lending formula: It isn’t all about credit score. A person who has a good job and secondary degree may get approved with Upstart when they might not with another lending platform.

- Receive money quickly: You can receive money as quickly as one day after accepting the loan.

- The low range of the APR is competitive: If you qualify for the lower end of the APR, that’s an attractive rate for a personal loan.

- A wide range of loan amounts: Whether you need a small loan or a sizeable balance, Upstart might be able to help you. A loan of $50,000, which is the max, can help you clean up credit card balances, medical expenses, or debt consolidation.

- It uses a soft pull for inquiries: You won’t have a hard pull on your credit score unless you decide to accept the loan. The soft pull won’t hurt your credit score.

- No prepayment penalty: If you want to retire your loan balance sooner, you can without facing a penalty with Upstart. That’s a plus for people who are motivated to pay off their debts as soon as possible.

- Can set up automated payments: These payments can save you time and will make sure you pay your installment every month by the due date.

- Gives you the opportunity to improve your credit score: If you accept the loan, your payment information will be sent to the credit bureaus, giving you the chance to boost your credit score if you handle your account responsibly.

Upstart Cons

- Charges an origination fee: That fee can be up to 8 percent, which is a bitter pill to swallow. There are a lot of personal loans out there that don’t charge an origination fee at all.

- Hard to be approved for people with low credit scores: If you don’t have at least a 620 credit score, you’ll have to look elsewhere for a loan.

- The APR can be really high: With the high side of the APR range at 35.99 percent, some applicants would pay more for a personal loan with Upstart than they might by keeping a balance on their credit card.

- Only two term lengths to choose from: Applicants only have a 3- or 5-year term to choose from. That doesn’t give much flexibility for borrowers.

Upstart Frequently Asked Questions

When people are considering using Upstart, they often have some questions. Here are some of the most common ones.

- Can I get a second Upstart loan while still paying on the first one?

- Can I get a loan with Upstart if I don’t have a credit score?

- How does Upstart decide who gets approved?

- How much income do I need to show to get a loan?

- How quickly can I receive funds?

Alternatives to Upstart

Before locking into anything, it’s always smart to consider all your other options for personal loans. We’ll compare some of the factors for other lending platforms you may be considering so you can make an informed choice.

| Upstart | Prosper | Upgrade | Avant | |

|---|---|---|---|---|

|

|

|

| ||

| Best For |

|

|

|

|

| Loan Amounts |

|

|

|

|

| APR |

|

|

|

|

| Minimum Credit |

|

|

|

|

| Terms |

|

|

|

|

| Origination Fee |

|

|

|

|

| Funding Speed |

|

|

|

|

| Credit Check |

|

|

|

|

Author:

Shannon is a mother of two and an award-winning journalist and freelancer who lives in Illinois. She obtained a bachelor’s degree in English from Illinois Wesleyan University before beginning her 20-year career in newspapers. When she’s not spending time with her children, she is often pursuing her favorite hobbies — running, metal detecting, kayaking, and reading about personal finance.

Reviewer:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.