Outlet Finance Review: Can You REALLY Earn 6% in a “Savings” Account?

Cryptocurrency-

Outlet Finance

Outlet Finance- Basics: Outlet brands itself as an alternative to savings accounts, but it’s more of a crypto lending platform than a traditional way to save. You could earn excellent returns compared to a conventional savings account, but results will be less predictable and you won’t have access to the same FDIC insurance.

- Pros: The interest rate is substantially higher than any savings account is currently offering, and Outlet seems to provide somewhat reliable coverage for smart contract hacks. The app is sleek and intuitive, and you can easily connect Outlet to accounts at thousands of banks through Plaid.

- Cons: Since Outlet doesn’t offer any FDIC coverage, you won’t be insured if they go under. The service is also built on crypto lending, so your returns are tied to the performance of digital assets like Ethereum rather than the value of the dollar or another traditional currency. Outlet can only be accessed through the mobile app, available on iOS and Android.

- FDIC Insured

No

- Mobile Deposit

Yes

- Bill Pay

No

- Minimum Balance

None

We may receive a commission if you sign up or purchase through links on this page. Here's more information.

If you’ve been following Money Done Right or my YouTube channel, you may have seen that my stimulus videos started generating a lot of views compared to what I was getting before. So now that my YouTube channel is approaching 100,000 subscribers I am getting hit up left and right by potential sponsors who want to pitch their products on my channel.

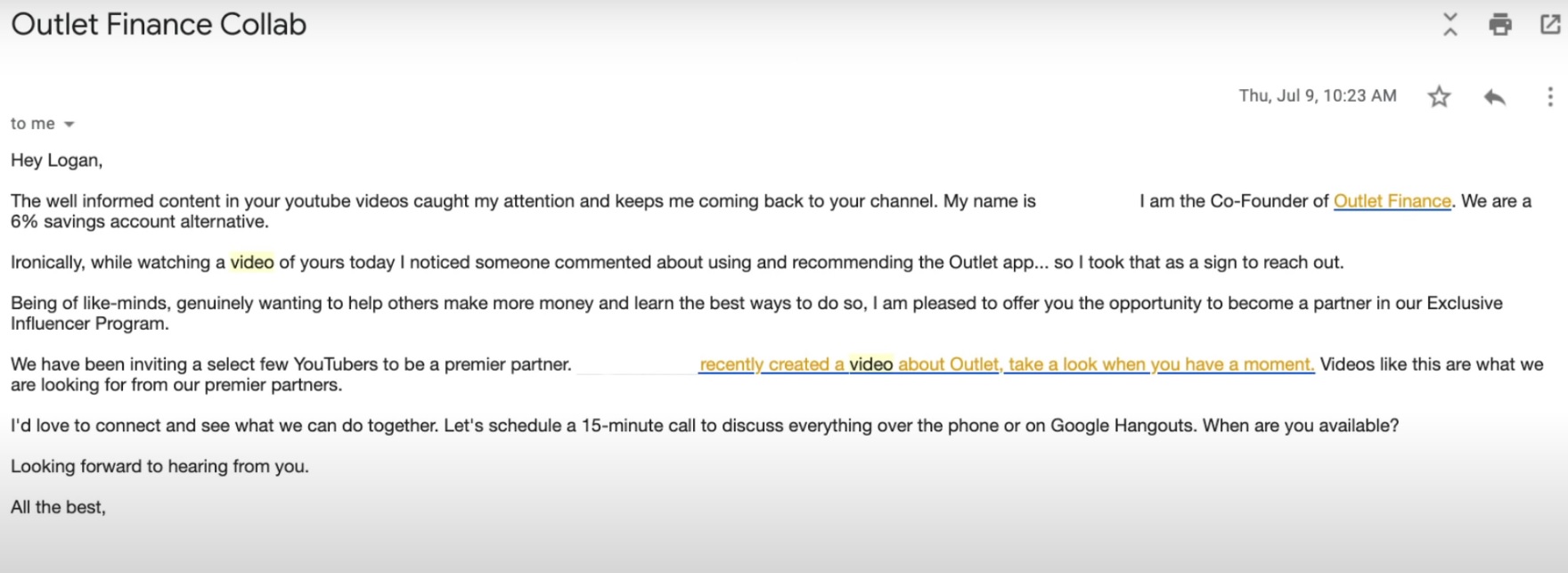

Here’s an example email I just received a few days ago:

OK, alright, so I look at this, and I think wow, 6% in a savings account “alternative,” that’s interesting to say the least, if it’s legit I would want to promote it. I mean you could earn more in the stock market over the long run than 6%, but 6% in a savings account, which one would think is less risky than the stock market, that sounds great.

Table of Contents

What Is Outlet Finance?

So I decided to do a little bit of digging into this savings account “alternative”

I went to Outlet Finance’s website to discover what it’s really about…

Business Model

The first thing I noticed on the Outlet website is the claim that they give users more money by “cutting out middle men [sic].” This is a little surprising because the website also states that whatever you put in is routed directly to third parties. In other words, Outlet might get a cut, but they don’t actually hold on to your money. Of course this means Outlet is actually the middleman itself, so I’m not sure why they claim to be getting rid of middlemen. To me that sounds more like marketing rather than anything substantive.

Crypto Lending?

From there, I wanted to know where my money is going, who they’re working with, and how they can offer a 6 percent return. I found out that your Outlet funds are stored in ERC-20, which is an Ethereum token — if you don’t know, Ethereum is a kind of cryptocurrency kind of like Bitcoin. So immediately that’s a huge red flag for me to have no mention of cryptocurrencies in his email and then learn on the website that this is actually an Ethereum project.

No FDIC Coverage

But again I didn’t want to rush to judgement, so I tried to keep learning about their business model, and it turns out that Outlet savings accounts are not FDIC insured. The FDIC, or Federal Deposit Insurance Corporation, covers people with checking accounts, savings accounts, money market accounts, and other types of accounts for up to $250,000 in case the bank or financial institution is unable to pay out. So if your bank goes under and your account is insured by the FDIC, you’ll get full compensation for up to $250,000.

Outlet doesn’t have that insurance, so you won’t have any recourse if they go out of business. The app says that accounts are insured for up to $50,000, but again that coverage isn’t coming from the government. Let me read some of the details of that insurance, again this is from the Outlet website:

“Lending risks are mitigated due to the fact that the loans your money goes toward backing are all overcollateralized. Meaning that for every dollar our lending partners loan out there is over a dollar being held by them.

Let’s follow this example on how lending risks are mitigated. You give Outlet $100. We then give this money to our lending partner who has a loan with collateral worth $130. If the collateral price were to dip below the $100 + the rewarded interest we liquidate the loan, and make sure that the lender (Outlet user) is made whole. This ensures that any funds loaned on Outlet are safe from default.”

The app actually says that accounts are covered for up to $50,000, but I couldn’t find any more information about the limits or restrictions of the coverage. Obviously that’s another big downside for Outlet compared to conventional savings accounts.

Is Outlet Really a Savings Account?

The easiest way to describe this model is that you give your money to Outlet, they give it to a third-party lender, and you get some of the interest on their loans. Of course 6 percent is a really excellent return if it’s reliable, but there’s also a decent amount of risk involved. Basically Outlet tries to minimize those risks by working with lenders who have enough collateral to cover your investment. That’s great, it’s an interesting concept, but I’m not sure I would trust it to the same degree I would trust FDIC coverage, for example.

Nexus Mutual

It turns out that Outlet works with a company called Nexus Mutual for insurance, so I did a little more research on them to get a better idea of the coverage offered by Outlet Finance. This is a blockchain-based alternative to conventional insurance, so again it’s not quite what you would expect from typical savings account coverage. Nexus is designed to help multiple parties distribute the risks of smart contract failure without the need for a centralized insurance company.

What Are Smart Contracts?

Smart contracts are what Outlet and many other businesses use to verify conditions for certain actions. So for example the Outlet smart contract might be designed to return collateral for the loan if it drops below the initial value. Here’s a link to the Nexus website in case you want to read more about their model, but here’s one thing that stood out to me about their product, which is called Smart Contract Cover:

“The Mutual may pay a claim under this Smart Contract Cover if:

- The designated smart contract address, or a directly related smart contract address in the case of a smart contract system, suffers a hack during the cover period that is a direct result of its smart contract code being used in an unintended way”

What that tells me is that Nexus insurance only applies to problems with the smart contracts themselves. So if for some reason you don’t get your collateral back, someone compromises Outlet, the system doesn’t work in some way, Nexus will help you recover what you should have received. On the other hand, if the collateral itself loses its value, whether it’s Ethereum or some other digital asset, you aren’t going to have any meaningful coverage. Sure you’ll get the money back in Ethereum, but that’s not really helpful if Ethereum is down 50 percent. Again this isn’t to say that you can’t earn good returns with Outlet, but your account won’t be covered in the same way a Bank of America savings account would be. Of course FDIC coverage depends on the dollar staying relevant, but that’s a lot more reliable than a currency like Ethereum.

Lending, Not Saving

Ultimately what Outlet offers is closer to lending rather than savings, and in my view they minimize the risks involved by branding themselves a “savings account alternative.” As the website says, it “looks, acts, and feels like a savings account,” but it’s important to clarify that it is not a savings account in the usual sense.

Is Outlet Worth It?

That said, Outlet is actually worth considering if you understand the risks and treat it as an investment and not a fairly secure way to hold your money like an FDIC-backed savings account. So I want to take a closer look at what Outlet offers and how it compares to some of the alternatives.

Mobile-only Access

First things first, Outlet really does look and feel like a savings account in some ways, and it advertises many of the features you would expect with an account from any other bank. The app is available on both the App Store and Google Play, but unfortunately there’s no support for browser access. You can learn about Outlet on their website, but you’ll still have to download the app on your mobile device if you want to create an account. There’s also no dedicated iPad app, so it will just scale up the iPhone version if you try to access your account on an iPad. This could be a pretty significant drawback considering how many savings accounts and other financial services are available online, but it won’t be a big deal if you bank exclusively on your phone.

ACH Transfers

Now Outlet also supports ACH transfers, which are one of the most common methods of moving money from one account to another. You can connect another account through Plaid, which works with thousands of banks and financial institutions including Wells Fargo, Chase, and CitiBank. Personally I linked Outlet to my Bank of America account in just a few minutes. So you shouldn’t have any trouble getting Outlet to work with your existing account. That said, I want to flag that Outlet expects transfers to take five full business days to arrive in your account, so make sure to send your transfers in advance.

Interest and Referral Bonuses

When I created my Outlet account I saw that the annual interest rate was 8.34 percent, significantly higher than the 6 percent I found on the website. The interest rate could vary depending on market conditions so it’s hard to say what it will be at any given time. You’ll also get a credit for $5 every time you refer someone to Outlet, and they’ll get an additional $5 when they sign up. A lot of websites offer one or two bonuses, but Outlet provides unlimited bonuses, so you could actually make a surprising amount of money by making referrals. Just remember to give referrals your link, which you can find in the app, so they can connect their account to yours and make sure both of you get the credit.

Customer Support

Now one potential problem I noticed when I used the app is that Outlet doesn’t offer much information about its support services. I sent a question and got a response saying they would be back “tomorrow,” but it didn’t give me business hours, an estimated wait time, or any other information. So they got back to me the next day, but it didn’t feel very transparent. There are a few pre-set questions you can ask a bot, but Outlet really doesn’t provide much information, which is unfortunate considering how unusual their business model is. It would have been nice to learn more about the service and see a little more transparency.

All things considered, Outlet wasn’t exactly what I was expecting from a savings account alternative, but it still offers a lot of interesting features that make it a unique option in this space. Outlet promises a decent interest rate — that’s actually a return on something of a speculative investment — and doesn’t have any hidden fees that I could see. So like I mentioned earlier in the article, I would recommend thinking of Outlet as an investment account instead of as a savings account, especially if there’s a chance you’ll need the money in the near future. I wouldn’t keep my emergency fund or my retirement savings on Outlet, but I would consider throwing in some extra cash to diversify my portfolio.

Of course you don’t want too much of any individual investment in your portfolio, I wouldn’t put more than a small percentage into Outlet, and assuming you have your emergency fund make sure you have a solid portfolio of “normal” investments like index funds before you throw money into something more speculative like Outlet, you can also click this link to check out a video I put together on investing for beginners. Overall, Outlet is a potentially high-risk but also high-reward option that makes crypto lending more accessible to inexperienced users, but there are a few drawbacks or at least concerns which I hope I’ve made clear throughout this article. Thanks to everyone for reading and remember to stay tuned at Money Done Right or through my YouTube channel for more stimulus updates and personal finance content.

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.