-

Betterment

Betterment- Basics: Betterment is a robo-advisor designed to invest your money through an algorithm that’s based on your priorities. The platform is suitable for those who prefer a hands-off approach to investing, and those who want to view all of their financial accounts on one platform.

- Pros: Betterment’s investment algorithm has a holistic approach, the .25% management fee is reasonably affordable, there’s no investment minimum, and your money will most likely be invested towards low-cost index fund ETFs.

- Cons: You could do whatever Betterment is doing for you at no cost, the platform optimizes using their management services so there might be a potential conflict of interest, and there are confusing elements throughout the account setup process.

- Welcome Offer:

Fee waived for one month if you deposit at least $15,000 into your account within the first 45 days of opening

- Fees:

0.25% annual fee for Digital Investing and 0.40% annual fee for Premium Investing

- Minimum Investment:

$0

- App:

Yes

We may receive a commission if you sign up or purchase through links on this page. Here's more information.

Table of Contents

What Is Betterment?

Betterment is a robo-advisor that’s designed to invest your money with your overall financial life in mind.

It’s one of the most popular robo-advisors out there — but does it get the job done?

For this review, I actually tried investing through the Betterment app to see for myself.

In this article, I give you a full walkthrough of the Betterment platform, discuss Betterment’s pros and cons, and share a few examples of who the platform would or would not be a good fit for.

If you want to watch a video review of Betterment instead, check out my Youtube video below!

Sign-Up Bonus

Betterment charges a small fee to manage your money, but currently, if you deposit at least $15,000 into your account in your first 45 days, Betterment will waive that fee for your first month.

If you deposit at least $100,000, you’ll get six months free, and if you deposit at least $250,000, you’ll get one year free.

How Does Betterment Work?

Betterment is a robo-advisor service: You deposit money, and the platform will manage it for you in exchange for a fee.

You can essentially do everything that Betterment is doing by yourself, but that will require time, effort, and making periodic adjustments.

Betterment promises a hands-off, low-involvement relationship with investing.

Below is a more in-depth look at Betterment’s features.

Tax-Coordinated Portfolio

With Betterment, you can set up a tax-coordinated portfolio which claims to boost after-tax returns by up to 15% over 30 years.

Betterment does this by organizing your portfolio so that your investments generating the most taxable income are located in a tax-advantaged account (like an IRA), and your investments generating less taxable income are located in a taxable brokerage account.

I can’t personally speak to how effective this method is because I didn’t try it, but this sounds like a good option for those who want to start a retirement account with Betterment.

Tax-Loss Harvesting

Through tax-loss harvesting with Betterment, you can sell stocks at a capital loss to offset any of your capital gains throughout the year.

To do this, Betterment will automatically sell securities in your account with losses so you can use them on your tax return to reduce your capital gains taxes.

Overall, this concept promises to reduce the amount of taxes you will owe, however, be mindful that if you’re already in the zero-percent capital gains bracket, tax-loss harvesting wouldn’t make sense.

This is a tricky concept to understand, so don’t worry if you’re confused.

Related: What Is Tax-Loss Harvesting? A CPA Explains.

Wash-Sale Rules

Additionally, be aware of wash-sale rules when engaging in tax-loss harvesting. These rules prevent investors from taking a tax deduction from a wash sale.

A wash sale, defined by the Internal Revenue Service (IRS), is when an investor sells a stock or other security for a loss, and either 30 days before or after selling, proceeds to buy the same or a “substantially identical” stock.

Betterment circumvents this by reinvesting your money into an ETF that’s similar (but not identical to) the ETF you sold, or by implementing some of their more advanced tax-loss harvesting strategies.

Annual Fee

0.25%For digital investingMin. Investment

$0Intro Offer

First Month FreeIf you deposit at least $15,000 within 45 daysHow Betterment Invests Your Money

Betterment lets you choose which Betterment portfolio you’d like to use to invest your money. Below is a more in-depth look at each Betterment portfolio and their asset classes.

Betterment Core Portfolio

The Betterment Core Portfolio is Betterment’s standard investing portfolio.

It consists mostly of low-cost ETFs, and Betterment claims that it’s tax-efficient.

Below are the asset classes included and not included within Betterment’s Core Portfolio.

| Asset Class | Included in Betterment Core Portfolio? |

|---|---|

| Bonds | |

| Short-term treasury bonds | Included |

| Inflation-protected bonds | Included |

| Investment-grade bonds | Included |

| International bonds | Included |

| Municipal bonds | Included |

| Emerging market bonds | Included |

| Equities | |

| Developed market | Included |

| Emerging market | Included |

| Other | |

| Private equity | Not included |

| Commodities | Not included |

| Natural resources | Not included |

For more information about Betterment’s Core Portfolio and selection process, visit this page.

Betterment Socially Responsible Investing Portfolio

Betterment’s Socially Responsible Investing Portfolio is similar to the Core Portfolio, but is more focused towards ESG investing, or impact investing for sustainable causes.

There are three variations of this portfolio; members can choose to invest through the Broad Impact Portfolio, Climate Impact Portfolio, or the Social Impact Portfolio.

When creating each of these portfolios, Betterment replaced the below asset classes with an ESG alternative:

- U.S. Stocks

- Emerging Market Stocks

- Developed Market Stocks

- U.S. High Quality Bonds

- U.S. Investment Grade Corporate Bonds

Because not all asset classes can be replaced with an ESG alternative at this moment, all other components of Betterment’s Socially Responsible Investing Portfolio remain the same as Betterment’s Core Portfolio.

| Portfolio Name | Goals and Vision |

|---|---|

Smart Beta

Betterment offers a Smart Beta option for your portfolio, which increases your chances of receiving higher returns in exchange for taking on more risk.

The Smart Beta portfolio, which is managed by Goldman Sachs, is more heavily-weighted toward stocks who exhibit these four key factors:

- Good value

- High quality

- Low volatility

- Strong momentum

Academic research has shown that stocks with these characteristics tend to outperform the market over time.

Learn more about Betterment’s Smart Beta strategy here.

Flexible Portfolios

Through Betterment, you can adjust your individual asset class weights.

However, I’d only recommend this if you’re an experienced investor.

To learn more about this feature, click here.

BlackRock Target Income Portfolios

If you’re retired, Betterment also offers income portfolios from BlackRock Investment.

The Target Income portfolio is a 100% bond portfolio, so it makes sense for people who are trying to conserve the money they have. It wouldn’t make sense for someone who is still working-age, and will benefit from the higher growth potential of investing in stocks.

Features and Benefits

Below are highlights of Betterment’s most distinguishable features.

| 0.25% annual fee | |

| $0 | |

| Fee waived for one month if you deposit at least $15,000 within the first 45 days of opening your account. | |

| 0.10% APY (varies) | |

| Traditional, Roth, and SEP IRAs | |

Betterment Checking Account

A Betterment checking account is issued by nbkc bank, FDIC-insured up to $250k, and has worldwide reimbursement for ATM fees.

After you sign up for this account, Betterment will send you a debit card which you can use at various places to get cash-back rewards through the Dosh cash-back platform.

Additionally, if you pay your cell phone bill with your Betterment Visa debit card, you can get up to $600 per cell phone claim for damage or theft with a $50 deductible (maximum of two claims per year).

Link External Accounts

Betterment allows you to sync external (non-Betterment) accounts, which is part of Betterment’s goal to integrate your whole financial life into one platform.

When you sync an external account to Betterment, you cannot manage it through Betterment, and Betterment cannot access that account to buy and sell as it pleases.

Rather, this feature is designed to help the platform “robo-advise” your Betterment-controlled assets.

You can also add your spouse’s accounts to Betterment to make sure their transactions won’t affect your tax-loss harvesting if you file jointly. And you can roll over an old retirement plan.

Betterment uses Plaid to link your external investment accounts.

I tested this out by attempting to link my M1 Finance account, and it worked pretty well. (If you’d like to learn more about M1 Finance, another robo-advisor, you can check out my review here.)

Cash-Reserve Account

Betterment’s Cash-Reserve Account is a high-yield savings account through the Betterment platform. It currently pays 0.10% APY, although this often fluctuates.

You can find high-yield savings accounts with higher APYs, but there are two benefits for signing up for the Betterment Cash Reserve:

- It integrates well with your other Betterment accounts because it’s already in Betterment.

- There are no limitations on moving money out of this account; Betterment claims to allow you to move your money as often as you want with no fees.

In contrast, most other high-yield savings accounts (and money market accounts) are restricted by Federal Reserve Board Regulation D, which says you can’t make more than six withdrawals or transfers out of your savings account per month.

College Fund Goals

For my college fund goals, Betterment prompted me to set up a taxable brokerage account that would be subject to a Betterment fee.

But from my experience as a CPA, a 529 Plan would be better for a college savings account – if you invest through a 529, your investments grow tax-deferred and your distributions towards education don’t get taxed.

Yet, Betterment makes no mention of setting up a 529.

This made me question whether Betterment has its users’ best interests at heart.

If I set up a platform like this, I would at least inform investors of the possibility of setting up a 529, even if I didn’t have a partnership with a 529 Plan provider.

Retirement Goals

In terms of retirement goals, Betterment offers Traditional, Roth, and SEP IRAs, which I’ll explain more about below.

You also have the option of setting up a taxable account (although I’m not sure why you would do that, since IRAs come with significant tax advantages).

Traditional IRA

If you’re eligible, a Traditional IRA offers a tax deduction for the money you put in now, and your investments can grow tax-deferred in the account.

After you turn 59 and a half years old, you can take money out of your account without a penalty. However, the money you remove will be subject to income tax.

Roth IRA

With a Roth IRA, you don’t get a deduction for the amount you put into your account, however, you can take money out tax-free once you reach 59 and a half. You can also withdraw contributions at any time without paying penalties or taxes. If you’re interested in learning more about Traditional IRAs and Roth IRAs, check out this post where I compare the two.

SEP IRA

And finally, a SEP IRA is similar to a Traditional IRA, but it’s designed for business owners.

Safety Net Goal/Emergency Fund

When signing up, Betterment asks you to set up a “safety net goal,” which is basically your emergency fund.

If you already have an emergency fund, you can just link that account to Betterment.

The safety net goal is different from Betterment’s Cash Reserve; an emergency fund should not be touched unless it’s an emergency, and the Cash Reserve should be used to fund your investments.

Net Worth

On your Betterment home screen, you can see your total net worth based on your linked accounts and Betterment balance.

I really like this integration feature within Betterment, since it also allows you to view a full breakdown of where your wealth is coming from.

Concierge Service

Betterment offers concierge service, which is designed to help you transfer assets from other accounts to Betterment without triggering any taxable events. This service is complimentary as long as you’re transferring at least $100,000.

Financial Advice

Betterment’s Financial Advice feature is for those who don’t have the Premium Investing plan, but are willing to pay hourly for a consultation with a CFP.

Betterment offers a variety of calls that you can book, including a 45-minute introductory call for $299 and hour-long calls on planning for retirement, college, marriage, etc., for $399.

Beneficiaries

Through Betterment, you can add a primary beneficiary.

Your primary beneficiary will gain control of the assets in your account if you pass away.

You can also add contingent beneficiaries, people who will gain control of your account if your primary beneficiary passes away before you.

Betterment Fees and Plans

Below are the different plans that you can sign up for through Betterment.

| $0 Annual Fee | 0.25% Annual Fee | 0.40% Annual Fee |

| $0 Minimum | $0 Minimum | $100,000 Minimum |

Checking Account

|

Betterment Checking Account and Cash Reserve

Betterment’s checking account and Cash Reserve requires no minimum deposit or fees. Additionally, you can always add these accounts to your investing plans for no additional costs.

Digital Investing

Digital Investing, Betterment’s default investing option, charges a 0.25% annual fee with no required minimum deposit.

For example, if you sign up for the Digital Investing plan and deposit $1,000 in your portfolio, your fee is $2.50 a year, whereas if you have $10,000 in Betterment, your fee is $25 a year, and so on.

Premium Investing

Betterment’s Premium Investing, available for those with at least $100,000 in Betterment, charges a 0.40% annual fee. For example, if you have $100,000 in your Premium Investing account, your annual fee will be $400, and so on.

This plan comes with all the features of the Digital Investing plan but also offers unlimited access to Betterment’s Certified Financial Planners (CFPs).

I have no personal experience with Betterment’s CFPs, but this price seems relatively affordable in exchange for unlimited access to a CFP.

Both the Digital Investing and Premium Investing accounts give you the option to choose between Betterment’s Core Portfolio or Betterment’s Socially Responsible Portfolio.

Is Betterment Safe?

Betterment is not a scam; it’s a safe and legitimate platform that was founded in 2010 by Jon Stein and Eli Broverman.

As of 2021, Betterment has a customer base of more than 650,000 investors and $32 billion in managed assets.

But if you’re wondering whether or not Betterment gives safe returns, note that any investment you make carries risk.

It’s impossible to know if Betterment will actually deliver a high return, but know that historically, investments do better when you buy and hold.

Betterment Pros and Cons

Now that I’ve gone over Betterment’s features, here’s what I liked and didn’t like about using Betterment.

Pros

- Holistic Approach: This can also be a con, since Betterment uses this to make money off of you, but in my opinion, Betterment’s platform is very convenient if you want to view your financial situation from a bird’s-eye perspective.

- Low and Affordable Fees: For a 0.25% fee, Betterment’s Digital Investing option manages your investments, adjusts your portfolio, and provides you with tax-coordinated opportunities. This seems like a reasonable fee to me, and the Premium Investing plan also seems affordable at 0.40%.

- Low-Cost Investment Options: Betterment mostly invests your money in low-cost index fund ETFs — particularly, Vanguard ETFs. I’m a big fan of Vanguard, so this is a plus in my book.

- No Account Minimums: You can get started on Betterment today even if you don’t have any money to deposit. This allows you to set up an account and make deposits in the future with whatever money you have.

- Sophisticated Tax-Planning: Betterment offers higher-level tax planning techniques such as tax-loss harvesting and a tax-coordinated portfolio.

Cons

- Charges For Things You Could Do Yourself: Betterment charges you to do things that you could do for free on your own. However, this is the same situation with most robo-advisors. When it comes to investing — if you know how and if you have the time — you can do it yourself.

- Potential Conflicts of Interest: Betterment wants to manage as much of your money as possible. This creates a conflict of interest between what’s best for you and what’s best for Betterment. For example, when I tried to set up an education goal, Betterment didn’t mention the possibility of setting up a 529 Plan, and instead tried to funnel me directly into a taxable brokerage account that it could manage. This results in you potentially losing out on better returns.

- Somewhat Confusing Setup: I was frustrated by certain aspects of the setup process. For example, when I had to input a target amount, Betterment didn’t allow me to set a date to hit that target amount by. Instead, after I finished setting up my account, it assigned me a target date of 2054, which I couldn’t adjust. There were several other confusing elements too, so in my opinion, Betterment needs to make a few changes to their setup process.

How is Betterment Different?

Betterment is different because it offers advanced investing strategies for relatively low fees, and it requires no minimum deposit to do so.

Similar services with low fees don’t all offer these strategies with direct access to CFPs.

Additionally, services or brokerages that offer to implement these strategies typically charge much more.

This is a pretty revolutionary concept, considering that this makes investing accessible to virtually anyone.

Betterment Alternatives

Betterment isn’t the only robo-advisor on the market.

In fact, a few alternatives to Betterment are Wealthfront, Charles Schwab, and Ellevest – and they all offer similar services with low fees.

Below is a table detailing each platform’s default investment options.

| Betterment | Wealthfront | Schwab Intelligent Portfolios (Charles Schwab) | Ellevest | |

|---|---|---|---|---|

| Fees |

|

|

|

|

| Account Minimum |

|

|

|

|

| Sign-up Offer |

|

|

|

|

| Features |

|

|

|

|

Betterment vs. Wealthfront

Betterment and Wealthfront both charge a 0.25% annual fee for their digital investing accounts, and both offer similar features good for set-it-and-forget-it investors such as tax-advantaged portfolios and financially holistic user interfaces.

However, there are a few key differences.

Betterment does not require a minimum deposit to start investing, and is more focused towards goal-setting and providing clients with one-to-one financial advice with a CFP for an upgraded cost.

Wealthfront requires a $500 deposit to start investing and you can’t get one-to-one financial planning support.

However, they do make up for the lack of in-person financial support with having a robust digital planning software.

Additionally, you can open a 529 college plan with Wealthfront – a feature that Betterment does not offer.

In my opinion, Betterment and Wealthfront are both reliable and trustworthy robo-advisors, so it all really comes down to what type of account you want to open, and how you want to invest.

Is Betterment Worth It?

Who Betterment Is Good For

Betterment is good for those who want to view all of their accounts in one place, those who fall within a higher tax bracket, and those who just want to set it and forget it.

If You Want To View All of Your Accounts In One Place

Betterment would be a good fit for those who want to view all of their financial accounts all at once.

Betterment houses all your accounts under one roof, and it can advise you on how to manage all of it from one place.

If You Fall Within a Higher Tax Bracket

If you fall within a higher tax bracket, you could benefit from Betterment’s automated tax tools.

While those in lower tax brackets could also benefit from Betterment, these additional features are particularly well suited to those in higher tax brackets who already have a bit of wealth.

If You Just Want to Set It and Forget It

Betterment may be a good fit for you if you’re looking to do set-it-and-forget-it investing.

With Betterment, all you have to do is deposit your money and Betterment will manage it for you with minimal involvement.

Who Betterment Is Not Good For

I would not recommend Betterment to those who don’t want to pay to have their investments managed, and to those who are active day traders.

If You Want To Manage Your Own Investments For Free

If you are extremely fee-sensitive and are willing to manage your own investments, Betterment is probably not a good fit for you.

As I’ve mentioned before, anything you can do in Betterment you can do yourself for free; Betterment just does it all for you in a single place.

If You’d Rather Day Trade

Betterment is also not a good fit for you if you want to engage in active trading.

As previously mentioned in this article, Betterment is a robo-advisor, which means that it automatically invests your money based on its algorithm.

With Betterment, investors are unable to specifically choose where their money goes.

How to Use Betterment (Step-by-Step Guide)

To set up your Betterment account, you can click this link, which will take you to the Betterment home screen, where it says “Start Investing and Get Up to One Year Managed Free.”

Step 1: Create your main account.

To set up your account, click “Get started”, input your email address, first name and last name, phone number, and a password and then click “Create account.”

In this example, I’m setting up an account for my wife (with her permission) since I already have a Betterment account and am unable to open another one.

Step 2: Create your other accounts.

At this point, you’ve set up a Betterment account, but once in Betterment, you have to create the separate accounts you want, whether a brokerage account, checking account, retirement account, etc.

To set up a taxable brokerage account for investing like I did, click “Finish setup” and then input more information including your address, city, state, date of birth, SSN, employment status, tax filing status, income and investment account balances, etc.

This is completely normal and is required to set up a brokerage account in the United States. Finally, click “Accept and finish” and then click “Goal setup” to tell Betterment what you’re going to use this account for.

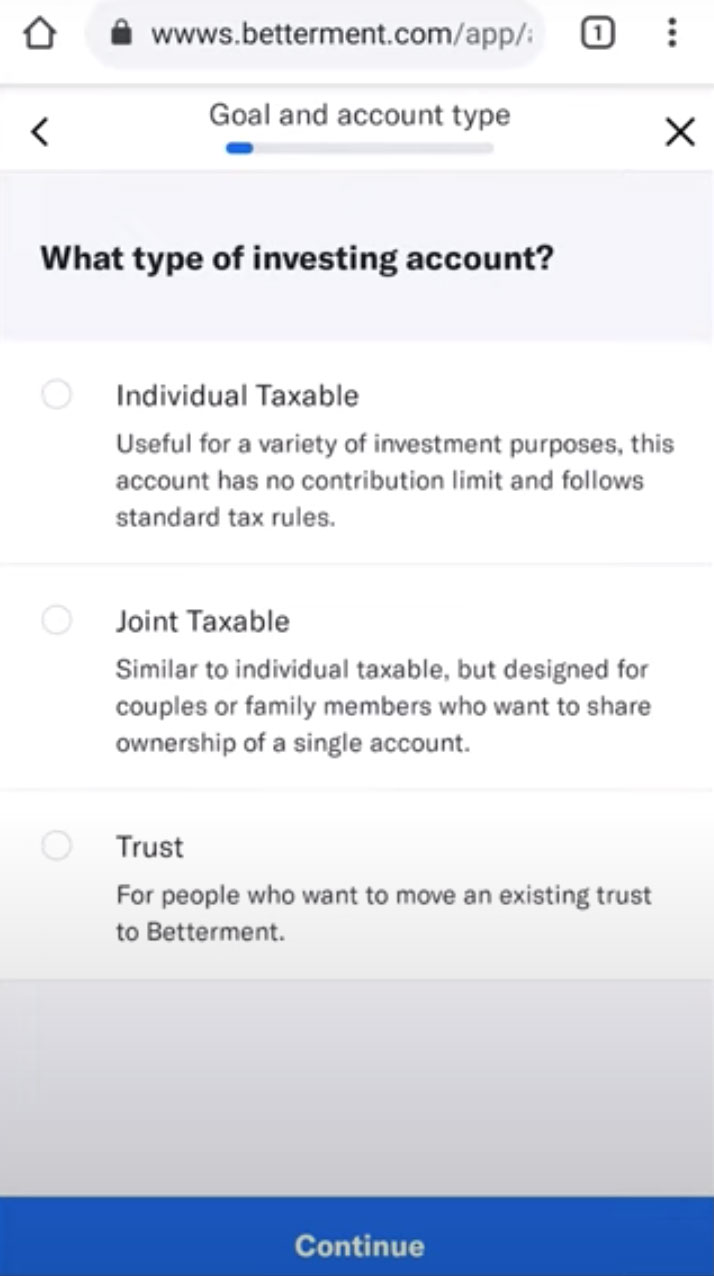

Account Ownership

In this case, the account is just for “General investing”, which has three separate categories of “Individual Taxable”, “Joint Taxable”, and “Trust”.

In this example, I selected “Individual Taxable”, but you can also select one of the other options.

Note that you are unable to create a trust through Betterment, so “Trust” is for those who already have an existing trust.

“Joint Taxable” allows for some easy estate planning and also comes with survivorship rights, meaning that if one of the account owners dies, the ownership of the entire account goes to the surviving owner.

Betterment allows you to set up a joint account even if you’re not married.

If I was going to use this account frequently, I would set up a joint account, but I chose “Individual Taxable” for the sake of this example.

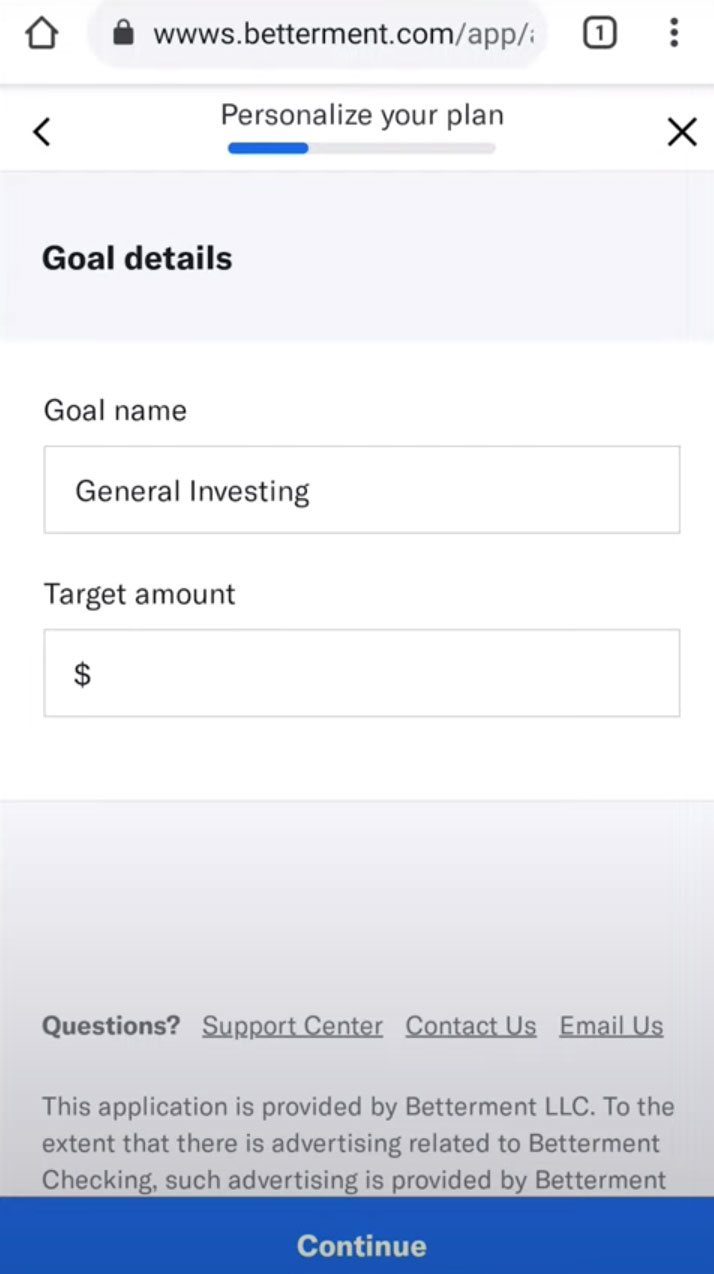

Account Naming and Target Amounts

You then click “Continue” and can name your account and select a target amount.

However, Betterment doesn’t attach a date to the target amount, which is frustrating, since someone might want to target a small amount now and a larger amount at some point farther in the future.

After clicking “Continue” again, you can also adjust your goal image.

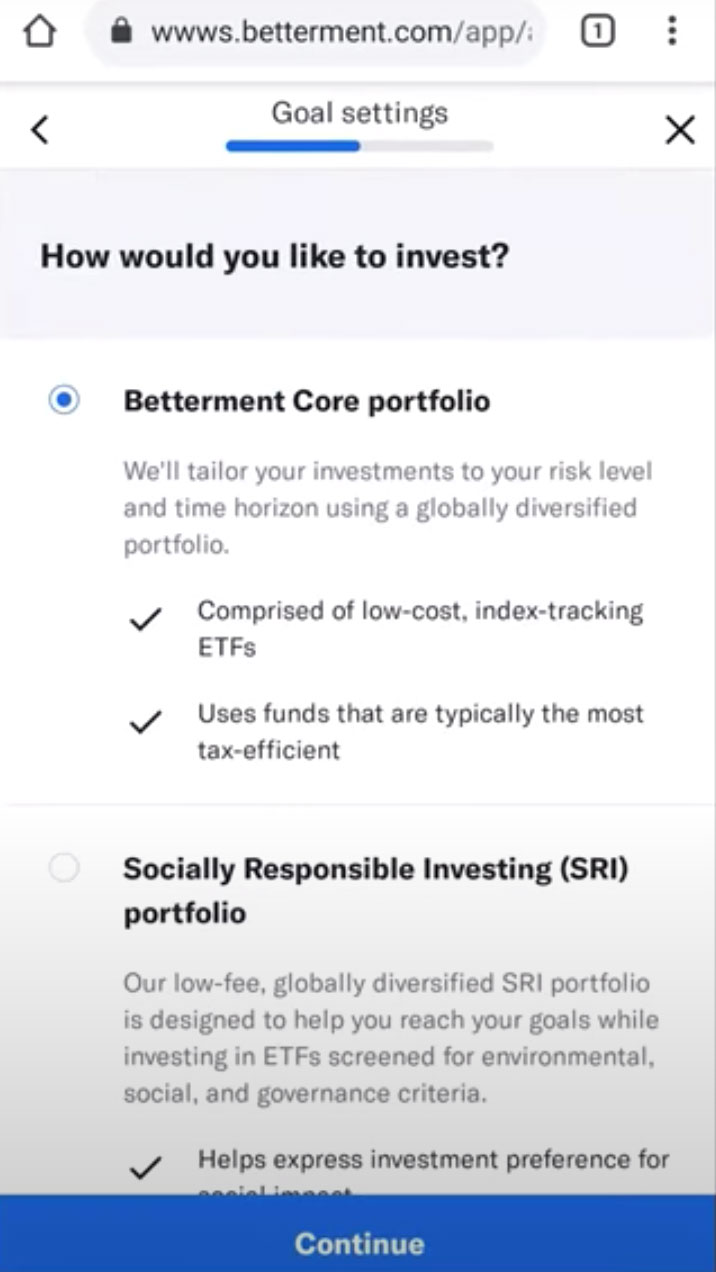

Step 3: Design your Betterment portfolio.

After clicking “Continue” one more time, you’ll see a screen saying, “How would you like to invest?”

At this point, you can start making some decisions about your Betterment portfolio. I’ve described some of the various options earlier in this piece.

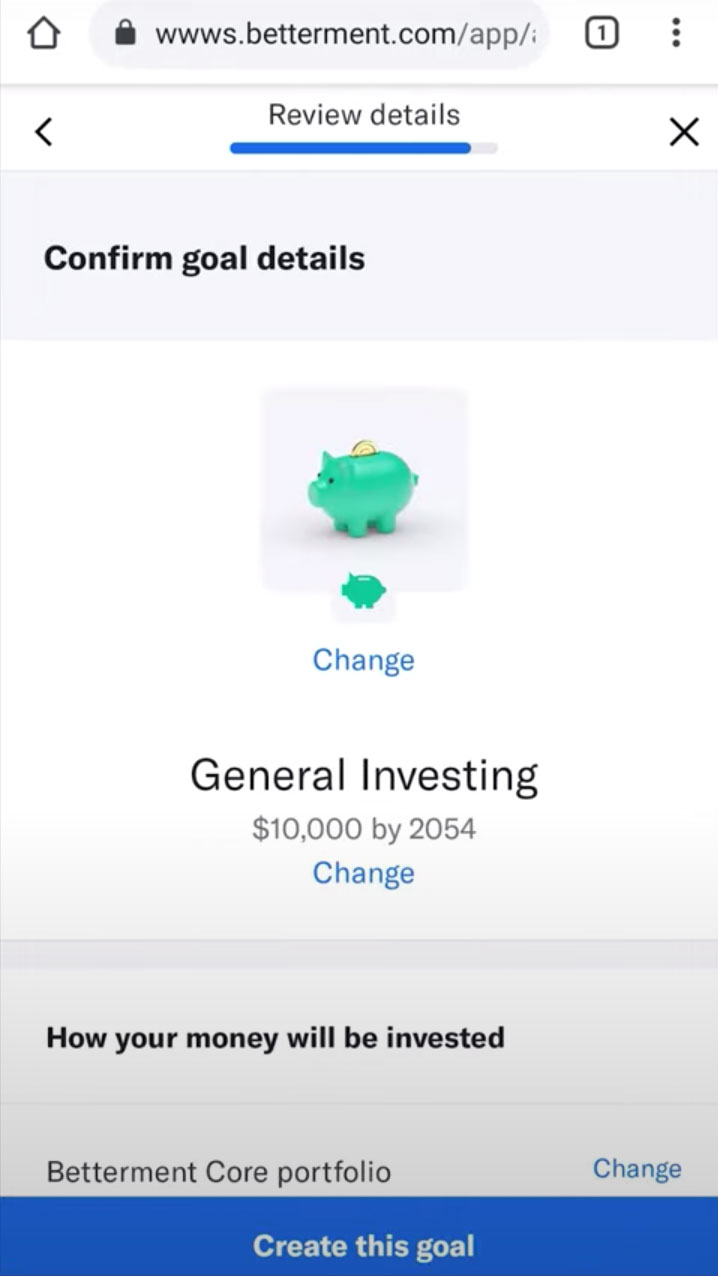

After choosing your portfolio, click “Continue”, and you’ll then see a screen saying “Confirm goal details”.

On this screen, you can see your target amount, along with the target date created for you by Betterment based on your estimated date of retirement (the year you’ll turn 65).

Unfortunately, Betterment doesn’t allow you to adjust this date in any way, and does not inform you of this date earlier in the setup process.

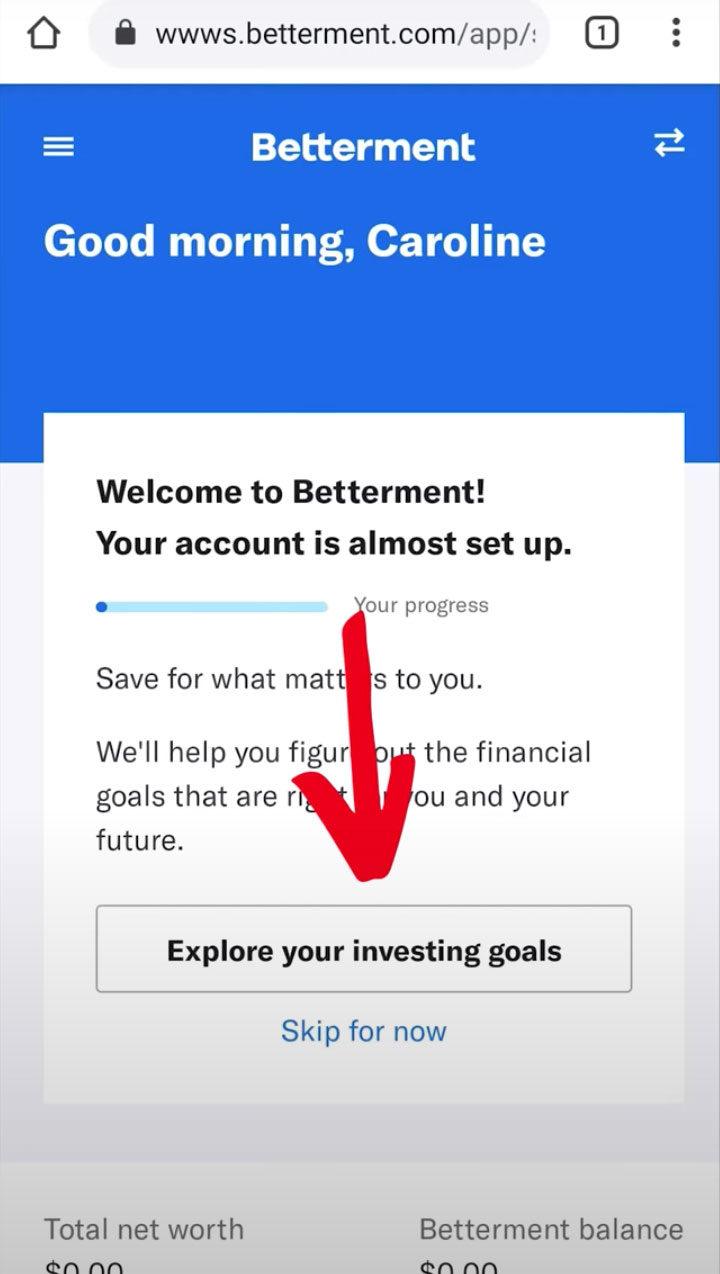

Step 4: Set up investing goals.

After reviewing everything on the “confirm goal details” screen, you can move on to setting up your investing goals.

First, you confirm what you told Betterment, then you tell Betterment about your children, home, and investing goals.

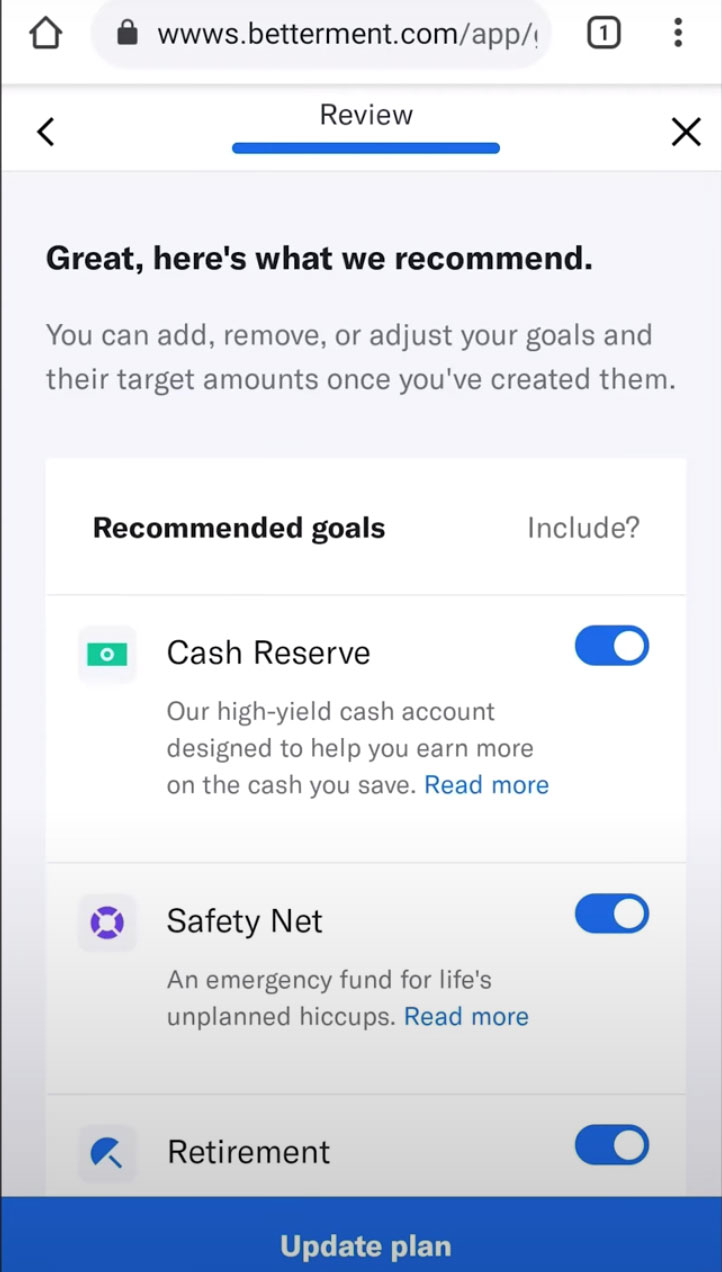

After this, Betterment gives you recommendations for the different account types you should set up (they call them goals because they might not technically be separate accounts).

In my case, Betterment recommended a cash reserve, emergency fund, retirement account, and college funds for our children.

Note that Betterment doesn’t necessarily say you need to set up these various accounts with them.

For example, in the case of retirement, Betterment says you can “sync non-Betterment accounts, like your current 401(k), to get holistic advice on allocations, funds, the right amount to save, and which account types to use to help maximize your money.”

This speaks to Betterment’s holistic nature; with other investing platforms like Robinhood, you just buy and sell stocks, whereas Betterment attempts to give you a comprehensive analysis of not just the funds you have at Betterment but your entire financial picture.

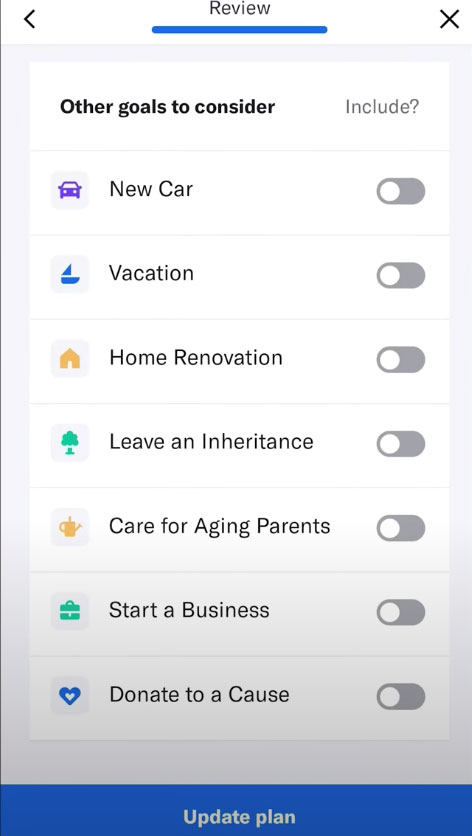

You can also add other goals in Betterment, like saving for a new car, home renovation, etc. I just picked vacation.

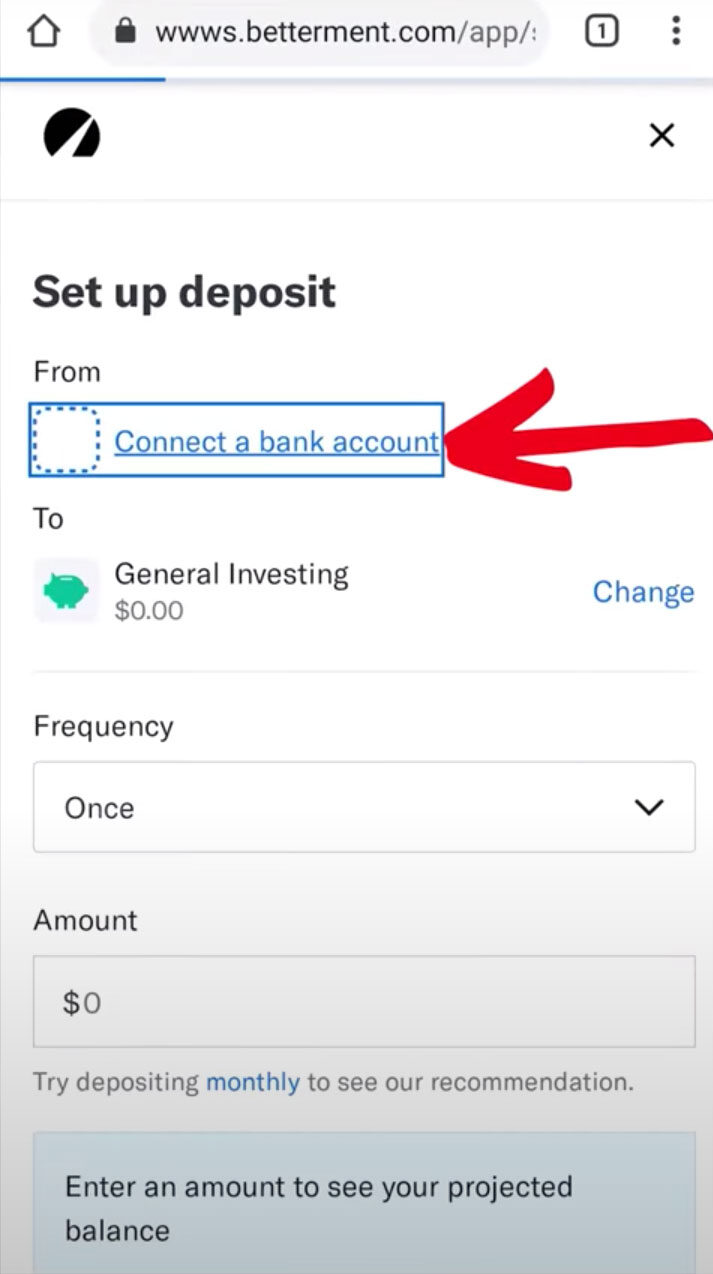

Step 5: Make your initial deposit.

After completing all these steps, you can make an initial deposit into your Betterment account by clicking “make a deposit”.

Betterment will first ask you to verify your email, after which you can click “Connect a bank account”, and then follow the standard procedure to connect your bank account through Plaid.

After connecting your bank account, you can set up your deposit.

In order to analyze this platform better, I chose to set up a monthly deposit of $100.

At the bottom of this screen, Betterment projects your balance at your target year, probably based on historical averages.

According to Betterment, based on these historical averages for this type of portfolio, my monthly deposits of $100 until 2054 (a total of $39,600) will ultimately equal $126,255.92 in 2054, showing how much money can grow over time.

After reviewing your deposit, clicking “Submit Deposit”, and completing a few more prompts, you’re all finished setting up your Betterment account!

Step 6: Explore the app.

The menu at the top allows you access to “Deposit”, “Transfer or rollover”, and “Refer a friend”.

These are pretty straightforward; “deposit” allows you to deposit your money, “transfer or rollover” allows you to move an account to Betterment, withdraw money from your Betterment account to your bank account, or view your previous transfers, and “refer a friend” allows you to access Betterment’s referral program.

Referral Program

If you invite someone to Betterment and they sign up and fund an account, both of you get $5,000 managed free for a year, for a maximum of five referrals a year equalling up to $25,000 managed free a year.

Betterment’s fee on your investment accounts is 0.25% a year, so the annual fee on $5,000 is $12.50.

Thus, the maximum referral reward per year is $62.50, assuming you have $25,000 in your Betterment account that you would otherwise pay the annual fee on.

Betterment Prompts

On the top of the home page of your new Betterment account, Betterment offers you several prompts to enable additional features.

These features, such as a Betterment checking account, and socially-responsible investing, are discussed earlier in this post, in the Betterment Fees and Plans section.

Left Sidebar

If you scroll down, you can see your goals, along with several other items on the left sidebar of the main screen.

Most are pretty straightforward- under “Transfers”, you can initiate deposits or withdrawals to or from Betterment, under “Activity”, you can view your account activity, under “Refer a friend”, you can access the referral program, and under “Settings”, you can update your personal information, beneficiaries, external accounts, etc.

Documents

Under “Documents” you can find your statements, tax documents, and other documents, which can be extremely helpful in terms of tax planning.

For example, if you click “Tax documents” and then “Realized gain/loss”, Betterment generates your year-to-date securities sales report so you know how much you’ll have to report on your tax return. You can also download your cost basis in your investments and see a record of year-to-date dividends paid to your account.

Ask an Advisor

Under “Ask an Advisor”, Betterment offers two different services: concierge service, and financial planning.

See the Features & Benefits section of this blog post, where I discuss these services in depth.

Rewards

Under “Rewards”, you can access a few rewards that Betterment offers, including the cash-back through the Betterment Visa debit card that I discussed previously.

Final Thoughts on Betterment

Thanks for reading my review of the Betterment platform!

I hope my experience helped you gain understanding of whether or not this is the right robo-advisor for you.

Overall, I really like what Betterment has to offer for both new and experienced investors, and I’m impressed with the platform’s commitment to accessible investing options.

If you decide that Betterment is for you, feel free to sign up using my link.

If you sign up using this link, I’ll get a small commission at no cost to you, so I can keep making reviews like this.

If you’re interested in another low-maintenance investment platform that charges no fees but requires you to be more involved in the portfolio selection process, check out this review of M1 Finance.

And finally, if you’re interested in free stocks (who isn’t?) – I happen to know a few ways you can get some free stocks, right now.

Frequently Asked Questions

Here are short answers to common questions about Betterment.

- Is it safe to invest with Betterment?

- Is Betterment worth using?

- What is the average return on Betterment?

- Can you make money with Betterment?

- Is Betterment good for beginners?

- What bank owns Betterment?

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.