-

DiversyFund

DiversyFund- Basics: DiversyFund is a REIT (real estate investment trust) that offers a diversified portfolio of 13 different properties, most of which are multifamily residences.

- Pros: DiversyFund enables everyday investors to get into the commercial real estate market with as little as $500.

- Cons: Investors can’t withdraw their funds for five years after paying in, and it could take even longer depending on market conditions. I had some issues with customer support and finding updated information about the properties.

We may receive a commission if you sign up or purchase through links on this page. Here's more information.

Table of Contents

What Is DiversyFund?

DiversyFund is a real estate investment trust that currently holds a total of 13 properties.

Investors can gain exposure to the real estate market for as little as $500.

Rather than buying into specific properties, investors purchase shares in the fund, which reflects the performance of each of DiversyFund’s properties.

Dividends are automatically reinvested back into the fund, and investors can liquidate their shares at the end of a five-year waiting period.

DiversyFund gives investors the opportunity to earn dividends through rent, plus their share of any increase in value stemming from appreciation as well as any renovations made to each property.

DiversyFund At a Glance

| Minimum Investment | $500 |

| Annual Fees | Asset management: 2% of equity per year Offering and organization expense reimbursement: Up to 10% of equity Acquisition: 1-4% of the cost of acquired assets Finance: 1% of the amount of any loans Profit sharing: DiversyFund gets a cut of all gains over the preferred return of 7% |

| Target Returns | 10%-20% |

| Accreditation Required | No |

| Lock-Up Period | Five-year term, no early withdrawals |

| Property Types | Multifamily, student housing |

| Project Types | Renovations |

| Regions Invested In | United States |

| Tax Structure | REIT |

| Tax Document Provided | 1099-DIV |

| Dividend Reinvestment | All dividends reinvested |

| 1031 Exchange-Eligible | Yes |

| Mobile App | Yes |

How Does DiversyFund Work?

DiversyFund takes contributions from its users, invests in real estate properties over a five-year period, and distributes returns to investors at the end of that term.

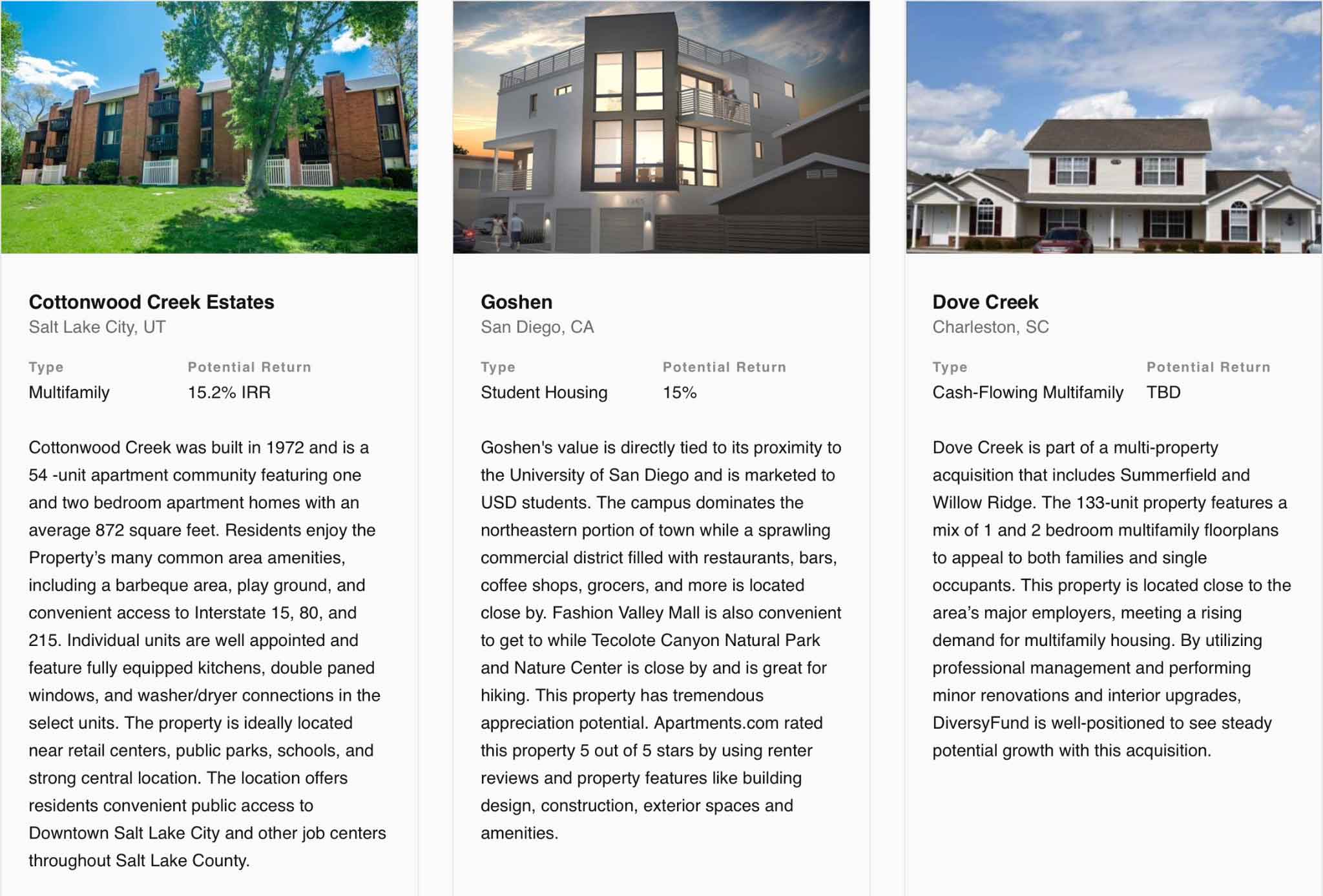

Property Types

DiversyFund is primarily focused on multifamily properties. My investment included 12 multifamily properties along with one student housing property.

In fact, DiversyFund is currently exclusively focused on apartment buildings. While there are 13 total properties, having so much invested in a single property type limits the fund’s overall diversification.

Property Locations

Properties are dispersed throughout the United States. I invested in three South Carolina properties, two North Carolina properties, two California properties, two Florida properties, two Texas properties, and two Utah properties.

DiversyFund had only released two REITs when I signed up, so it’s hard to say where its properties will be located in the future.

Project Types

Increasing the value and rent of each property through renovation is a key aspect of DiversyFund’s investment strategy. According to the DiversyFund website:

“We do what is called a value-add play. We add value to the properties via renovations. We renovate the individual units, common areas, etc. We utilize cash flow from the properties to fund the renovations over a period of time….We only acquire properties in areas with strong job growth and population growth, and with vacancy rates below the national average.”

Target Returns

DiversyFund is aiming for an IRR (internal rate of return) of 10% to 20% for each property.

This is a strong target that would make DiversyFund competitive with the S&P 500 and other market indices.

Of course, there is no guarantee that investors will actually reach that target range or even recoup their initial investment.

Considering the substantial fees, each property would need to offer gross returns well over 10% in order for investors to see a 10% IRR.

Neither of DiversyFund’s REITs have been liquidated to date, and there is very limited information about recent changes in value, so I can’t say how realistic the platform’s projections are. Ultimately, you will have to make your own judgment about the investment’s potential based on the information provided by DiversyFund.

Minimum Investment

DiversyFund requires a minimum investment of $500.

Investment Duration and Lock-Up Period

Each DiversyFund REIT comes with a term of roughly five years. You won’t be able to withdraw your funds for at least five years after investing.

Since DiversyFund only pays out after selling its holdings, there’s a chance that you will still be unable to liquidate at the end of five years. Check the offering circular they filed with the SEC for more information.

Vetting and Review Process

Given DiversyFund’s goal of liquidating investments after five years, the team naturally looks for assets that match a five-year time horizon.

Many of the assets in the DiversyFund portfolio are already generating consistent cash flow at the time of the acquisition.

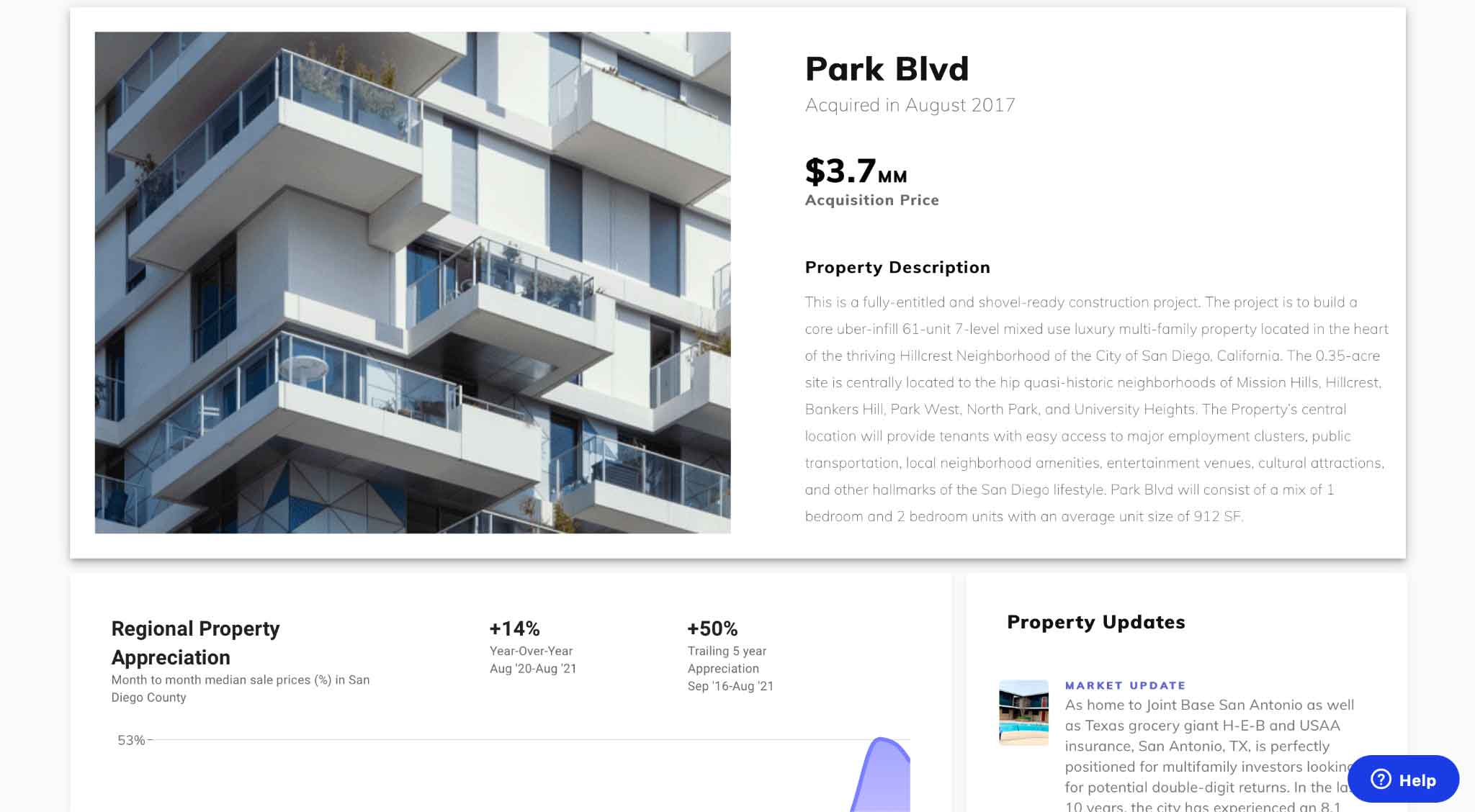

I also saw one project that involved building an entire apartment building in San Diego, so DiversyFund isn’t necessarily opposed to backing ground-up developments.

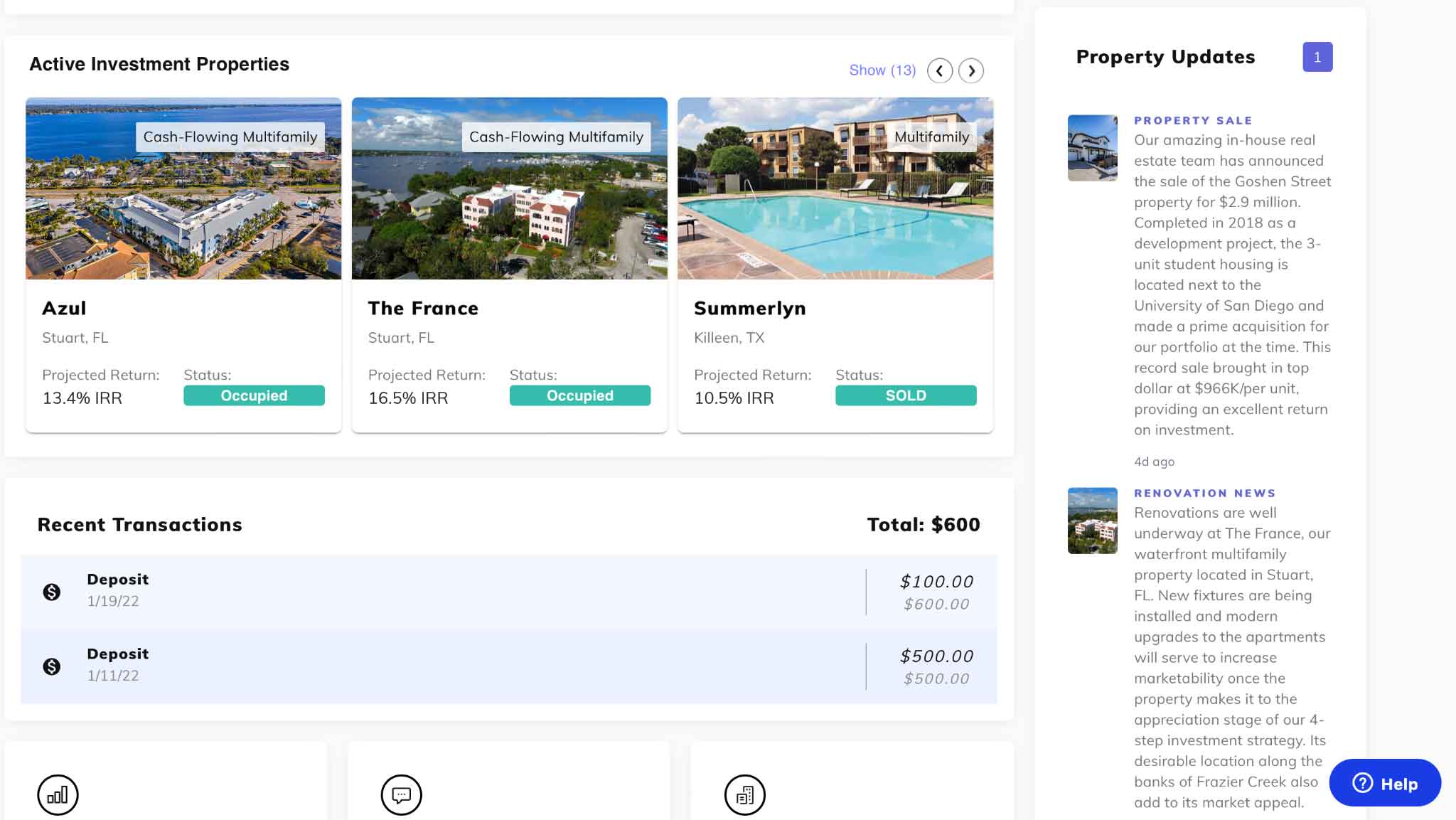

DiversyFund acquired this property more than four years before I signed up, so it was disappointing to see that the listing still contained just one picture, a generic blurb, and information about regional property information in the region.

While property updates are listed in the bottom-right corner, there’s no way to filter them to find information about specific properties. Overall, I felt that DiversyFund dropped the ball with respect to keeping investors informed about the way each project was going.

Tax Implications

Dividends are automatically reinvested, but you will still have to pay income tax on accrued dividends at the end of each year. On the other hand, you may also be able to take advantage of deductions from depreciation.

After properties are liquidated at the end of the term, you will pay capital gains tax on any positive returns over and above your initial investment.

Investors who earn more than $10 in dividends in a given tax year will receive a 1099-DIV form from DiversyFund early in the following year.

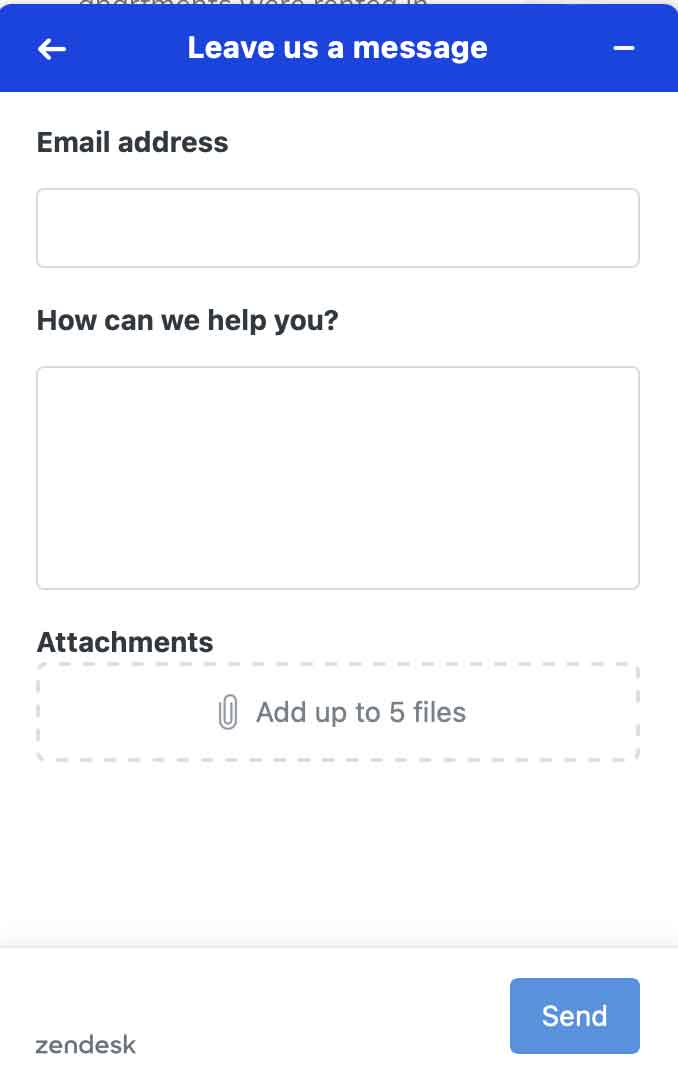

Customer Service

In response to customer reviews, DiversyFund has claimed that they respond to support requests within 1-3 hours.

However, the automated customer service email gives a totally different timeline, saying that “During 9:00 A.M. to 4:00 P.M. PT, we aim to respond within 48 hours.”

You can ask questions to the AI chatbot or leave a message and wait for the support team to contact you again via email.

DiversyFund took about seven hours to reply to my first message, which I sent a little before 9:00 A.M.

Unfortunately, the response I received didn’t offer any clarity with respect to our question. Instead, they simply sent a link to the page I had already referred to.

Even after I followed up, they never gave me the relevant information or even addressed my question directly. I eventually found what I wanted on my own, but the customer service team should have been able to point me in the right direction from the beginning

While your experience with support may be totally different, this interaction left me with even more concerns about DiversyFund’s investor relations.

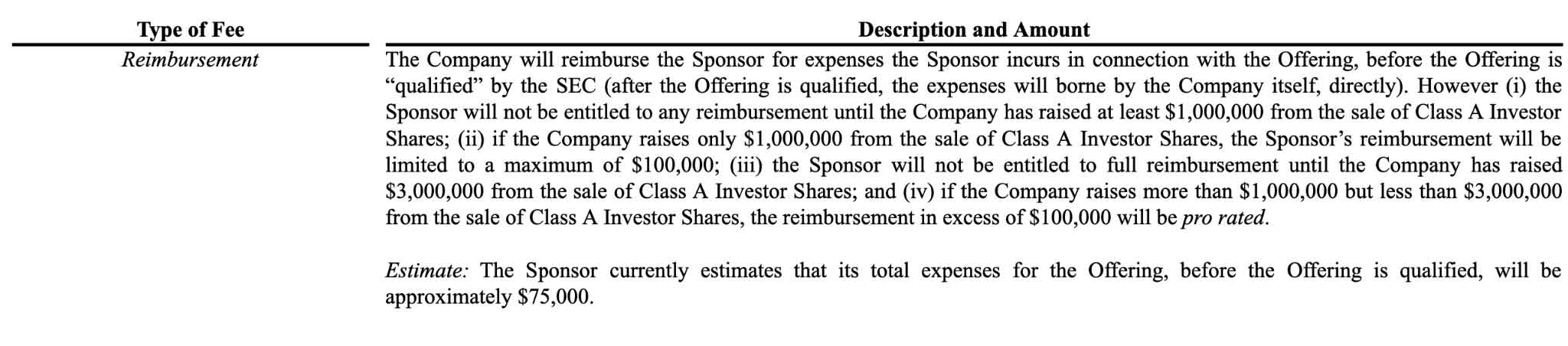

DiversyFund Fees

DiversyFund charges a number of different fees.

Asset Management Fee: DiversyFund comes with an asset management fee equivalent to 2% of gross operating income, typically the gross rental revenue.

Sponsor Fee: DiversyFund’s sponsor charges a fee of between 6% and 8% of total project costs, including hard costs like the cost of the property itself, as well as soft costs such as fees paid for professional services.

Property Disposition Fee: When DiversyFund or an entity owned by DiversyFund sells a property, the sponsor receives a property disposition fee worth 1% of the total sale price. There may also be a property disposition fee of up to 1% in the case of joint ventures.

Financing Fee: Similarly, the sponsor receives 1% of any loans placed on a particular property, either at the time of acquisition or later on in the case of refinancing. As with property disposition, there may also be a financing fee associated with joint ventures, but the sponsor will still not receive more than 1% of the loan value.

Construction Management Fee: In cases where the sponsor provides construction management services, it will receive a construction management fee worth 7.5% of the cost of construction.

Guaranty Fee: If the sponsor or one of its affiliates guarantees any debt taken on by DiversyFund, it will receive a guaranty fee equivalent to 0.5% of the debt.

The offering circular also includes a disclaimer about additional fees that may come up if the sponsor or an affiliate performs other services for DiversyFund:

“The compensation paid to the Sponsor or its affiliates in each case must be (i) fair to the Company and the Project Entities, (ii) comparable to the compensation that would be paid to an unrelated party, and (iii) disclosed to Investors.”

Finally, DiversyFund takes a cut of profits from the fund beyond the preferred return of 7%.

In other words, you won’t give up any returns up to 7% per year, but DiversyFund will get a substantial share of any profits beyond that threshold. This isn’t technically a fee, but it could still make a significant dent in your returns.

According to the offering circular, 100% of profits go to investors up to an IRR of 7%. Investors get 65% of profits until they reach an IRR of 12%, and 50% of all profits beyond that threshold.

| Internal Rate of Return | Proportion Distributed to Investors |

|---|---|

| Up to 7% | 100% |

| 7% to 12% | 65% |

| Beyond 12% | 50% |

While fees are common with REITs and other real estate investments, investors could lose a significant amount of money to all of these different charges.

DiversyFund’s fee structure makes it difficult to say exactly how much you’ll end up paying, either in real terms or as a percentage.

The 2% asset management fee, for example, only applies to rental income and not the value of the properties. In contrast, the property disposition fee applies to the full sale price of each property.

The preferred return also puts substantial limitations on the upside of DiversyFund.

Investors receive just 50% of returns beyond the 12% IRR, which means that they get a smaller and smaller share of the pie as the pie grows.

If the total returns work out to 20% IRR, for example, investors will keep the entire first 7%, 3.25% of the next 5%, and 4% of the last 8%. This means that 14.25% out of a total IRR of 20% will go to investors, who will also lose money on the other fees described above.

On the other hand, investors will give up a much larger portion of the returns if the total IRR works out to, say, 40%. In that case, investors would end up with just 24.25%, with 15.75% IRR being lost.

Is DiversyFund Legit?

The SEC qualified DiversyFund as a REIT (real estate investment trust) in November 2018 under regulation A.

Companies that make offerings under regulation A are not required to register with the SEC, but they are still required to file reports and submit to SEC audits.

In June 2019, the SEC also approved DiversyFund’s request to lower the minimum investment to $500 from the original $2,500.

Regulation A is commonly used by real estate investment platforms, so the fact that DiversyFund is exempt from SEC registration is no cause for concern. That said, it’s a good reminder for investors to do their own due diligence in evaluating the offering.

I also found that DiversyFund is accredited by the BBB and has a perfect A+ rating, although its customer review rating is a less impressive 3.61 out of 5.

Investors should remember that just because DiversyFund is a legit business doesn’t mean that its offering comes without risk or is guaranteed to achieve the company’s goals.

Real estate is an inherently risky investment, and DiversyFund only offers limited diversification with its portfolio of 13 properties.

Since there are no early withdrawals, investors will not be able to respond to changes in their outlook by liquidating their shares or adjusting their strategy.

Naturally, you should only invest in DiversyFund using money you can afford to lose, and at the very least afford to keep invested for a full five years.

| Reviewer | Experience | My Take |

|---|---|---|

| Fateh (BBB) | Fateh complained that DiversyFund was still raising money more than two years after the initial offering, contradicting the terms of the statement at the time. This appeared to extend the timeline without giving investors the opportunity to adjust their strategies.

DiversyFund response: “The Growth [REIT] filed a supplement with the SEC extending the offering to November 13, 2021 and increasing the raise amount to $75 [million]. The [REIT] can also file a new offering allowing it to raise an additional $75 [million] under Regulation A+.” | I assume the DiversyFund team is telling the truth about this being allowed, but it still seems notable that people bought in based on the two-year term from the first offering, then had the timeline changed on them after that without being able to access their money. I understand that they might not be able to liquidate in the desired five years, but it seems worse to change the acquisition period after giving investors information upfront that seemed to indicate the opposite. Also, their experience with customer service basically mirrors mine —I sent several emails and was never able to get anything other than a boilerplate response. |

| No name (BBB) | This user felt that DiversyFund deceived them by hiding the critical detail that investments are locked in for a period of roughly five years. They claimed that they wouldn’t have bought in if they had understood that restriction upfront.

DiversyFund response: “Since we are executing a growth strategy to maximize returns offering an early withdrawal actually impedes this. Therefore, to protect the growth of all our investors’ wealth there are no premature withdrawals….All of this is stated on the website and investors acknowledge and sign the investment agreement when processing the investment.” | I can see this one both ways. I don’t think it’s fair to say that DiversyFund “misled” this person, but the website is a little cagey about the five-year thing. It’s not mentioned at all on the homepage, and even the fund page only says things like “the value-add cycle is approximately five years” without specifically mentioning that investments are locked in for that entire period.

DiversyFund’s response mentions the investment agreement, but I signed the same document, and it doesn’t say that as clearly as the response implies. The closest thing is a passage that says “You understand that under the terms of the LLC agreement, the Shares may not be transferred without our consent….As a result, you should be prepared to hold the Shares indefinitely.”

On the other hand, the five-year holding period is explicitly covered in the FAQ. |

| David Shea (TrustPilot) | While David gave DiversyFund a relatively positive rating of 4 out of 5, he mentioned that it would be nice to be able to see more information about each individual property, including current performance and future projections. | David is right that the DiversyFund website is a little light on details. Even as an active investor, I was only able to see a short and relatively bland statement about the properties in my portfolio. For example:

“Summerfield is part of a three-property purchase that includes Willow Ridge and Dove Creek. Built in 2009, the property needs little maintenance and interior updating to produce increased potential return on investment.” |

DiversyFund Pros and Cons

DiversyFund is offering a strong target return with a minimum of just $500. That said, it comes with a number of fees plus a long-term commitment, and I was disappointed by the limited information it provides to investors.

Pros

Pros

- Minimum Investment: DiversyFund starts at just $500

- Accessibility: DiversyFund is open to both accredited and non-accredited investors.

- Potential Returns: DiversyFund is targeting an IRR (internal rate of return) of 10%-20%.

Cons

Cons

- Five-Year Term: No withdrawals before the end of the five-year term.

- Fees: You’ll pay fees for asset management, financing, and expenses, and DiversyFund will also take a share of all returns over 7%.

- Investor Relations: DiversyFund doesn’t offer much information about its properties, and I also had a negative experience with customer support.

Alternatives to DiversyFund

| DiversyFund | HappyNest | CrowdStreet | Streitwise | |

|---|---|---|---|---|

| Property Types |

|

|

|

|

| Property Locations |

|

|

|

|

| Target Returns |

|

|

|

|

| Minimum Investment |

|

|

|

|

| Minimum Duration |

|

|

|

|

| Accredited Investors Only? |

|

|

|

|

Is DiversyFund Worth It?

DiversyFund could be worth it if you’re looking for a way to put a chunk of your savings into real estate while giving yourself exposure to a number of different properties.

Who DiversyFund Is Best For

DiversyFund is ideal for people who can comfortably invest $500 or more knowing that they won’t be able to access that money until the end of the five-year term.

If you’re currently a renter rather than an owner, you’ve been getting the worse end of the real estate boom of the last ten years and beyond.

While increases in real estate value are good for owners, they only come to renters in the form of higher monthly expenses.

Investing in DiversyFund or another REIT could give you a hedge against the real estate market as a renter.

As long as you have some money invested in real estate, you’ll be able to take advantage of growth in the real estate market instead of simply paying more in rent.

Who DiversyFund Is Not For

DiversyFund is not for people who want liquid assets or who aren’t ready to put $500 into a real estate investment.

While real estate can be a great way to build wealth, it’s important to understand that DiversyFund requires a long-term commitment and comes with significant risk.

If you don’t have an emergency fund covering at least a few months of expenses, I recommend prioritizing your financial security over the potential gains from a more speculative investment.

Keep in mind that DiversyFund is operating on a five-year timeline and does not allow for any early withdrawals.

If there’s a chance that you’ll end up needing your funds back before the end of the five-year term, consider investing in something that offers more liquidity.

How to Use DiversyFund (Step-by-Step)

- Visit the DiversyFund website or download their mobile app, which is available for both iOS and Android.

- Sign up with your email address and password, or connect DiversyFund to your Google, LinkedIn, Facebook, or Apple account.

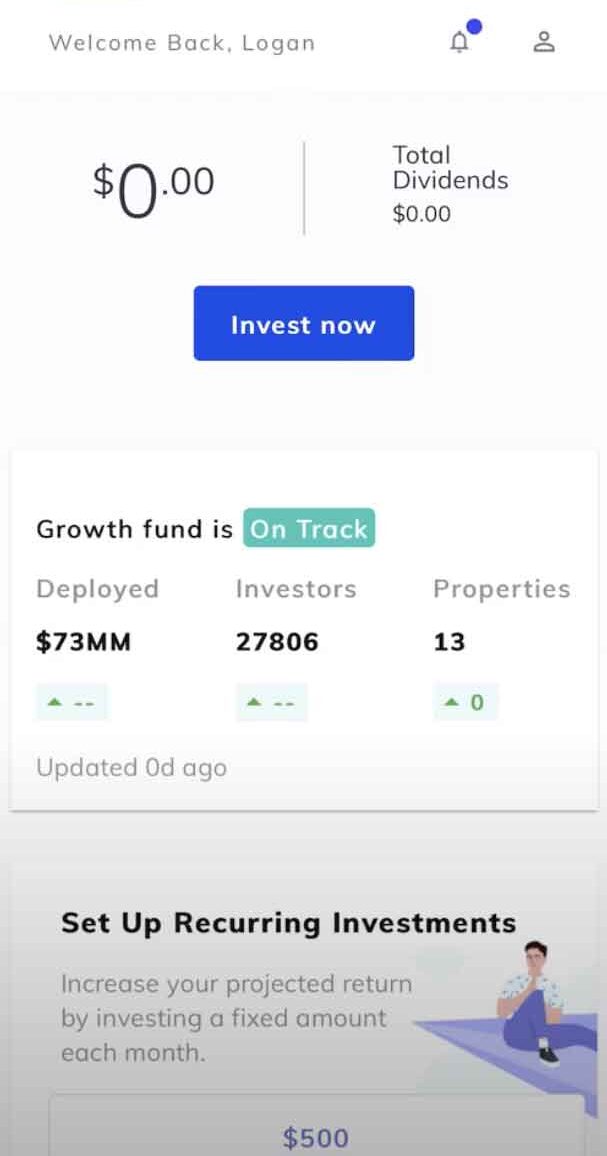

- Tap the “Invest now” button when you’re ready to make your first investment.

- Enter the required information such as your address, phone number, the size of your investment, and the type of account you’re planning to invest with. DiversyFund currently accepts investments of $500 to $1 million.

- Enter your bank information or link an account through Plaid. While I was able to input my details manually, DiversyFund had trouble pulling my account information from Plaid. The support team wasn’t able to identify the issue, but it doesn’t seem to be a common or recurring problem for other DiversyFund users.

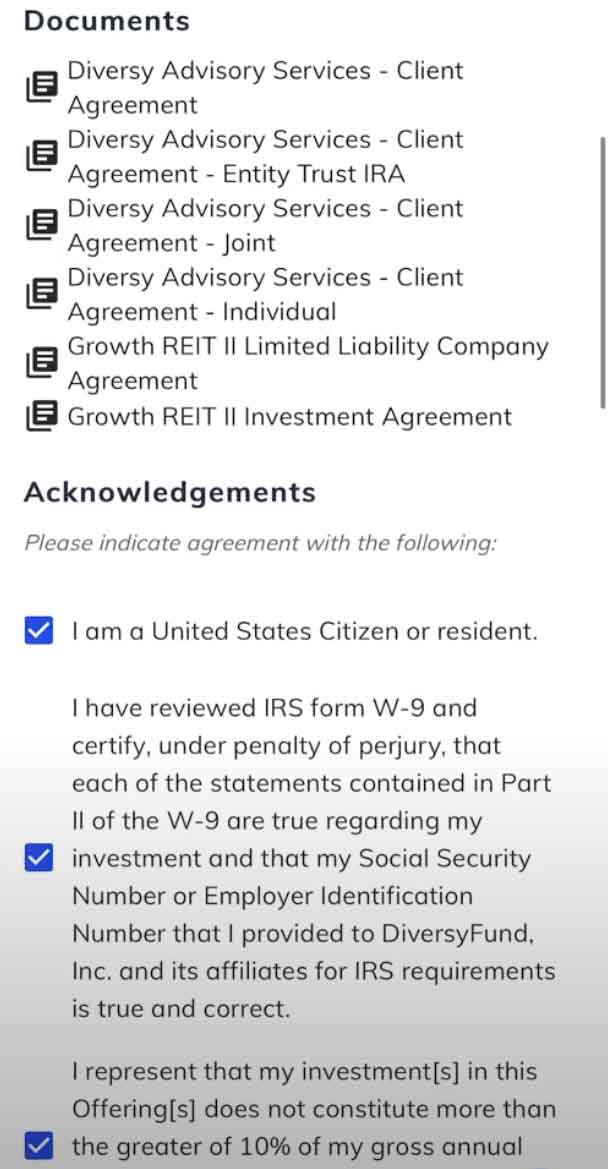

- Read through the DiversyFund agreements and confirm that you understand the requirements and risks.

- Enter your Social Security Number and date of birth to verify your identity and finalize the investment.

Final Thoughts

DiversyFund is one of many recent projects designed to make real estate more accessible to the average investor. While $500 isn’t an insignificant amount of money, it’s still a relatively low minimum investment for the real estate market.

The main downside of DiversyFund compared to most publicly traded REITs is its long holding period. You should only consider this opportunity if you’re prepared to keep your money invested for a full five years (and possibly longer).

However, reinvesting dividends and preventing early withdrawals may also help DiversyFund maximize its potential over the full term of the investment. Whether it makes sense for you to put money into DiversyFund ultimately depends on your unique investing strategy.

Frequently Asked Questions

- Do I have to be an accredited investor to invest in DiversyFund?

- How do I withdraw from DiversyFund?

- Who owns DiversyFund?

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.