-

HappyNest

HappyNest- Basics: HappyNest is a real estate investment trust (REIT) that gives investors access to the returns from three commercial properties in the eastern United States.

- Pros: Investors can get started for as little as $10, and HappyNest offers a well-reviewed mobile app that makes it easy to invest.

- Cons: Investors have to wait at least six months to withdraw, or three years to withdraw for full value. With returns based on just three properties, HappyNest doesn’t provide much diversification.

We may receive a commission if you sign up or purchase through links on this page. Here's more information.

Table of Contents

What Is HappyNest?

HappyNest is a real estate investment trust, or REIT, that distributes the returns from three commercial properties to its investors.

Investments can be redeemed for their full value after three years. The price of HappyNest shares varies depending on the value of the properties themselves.

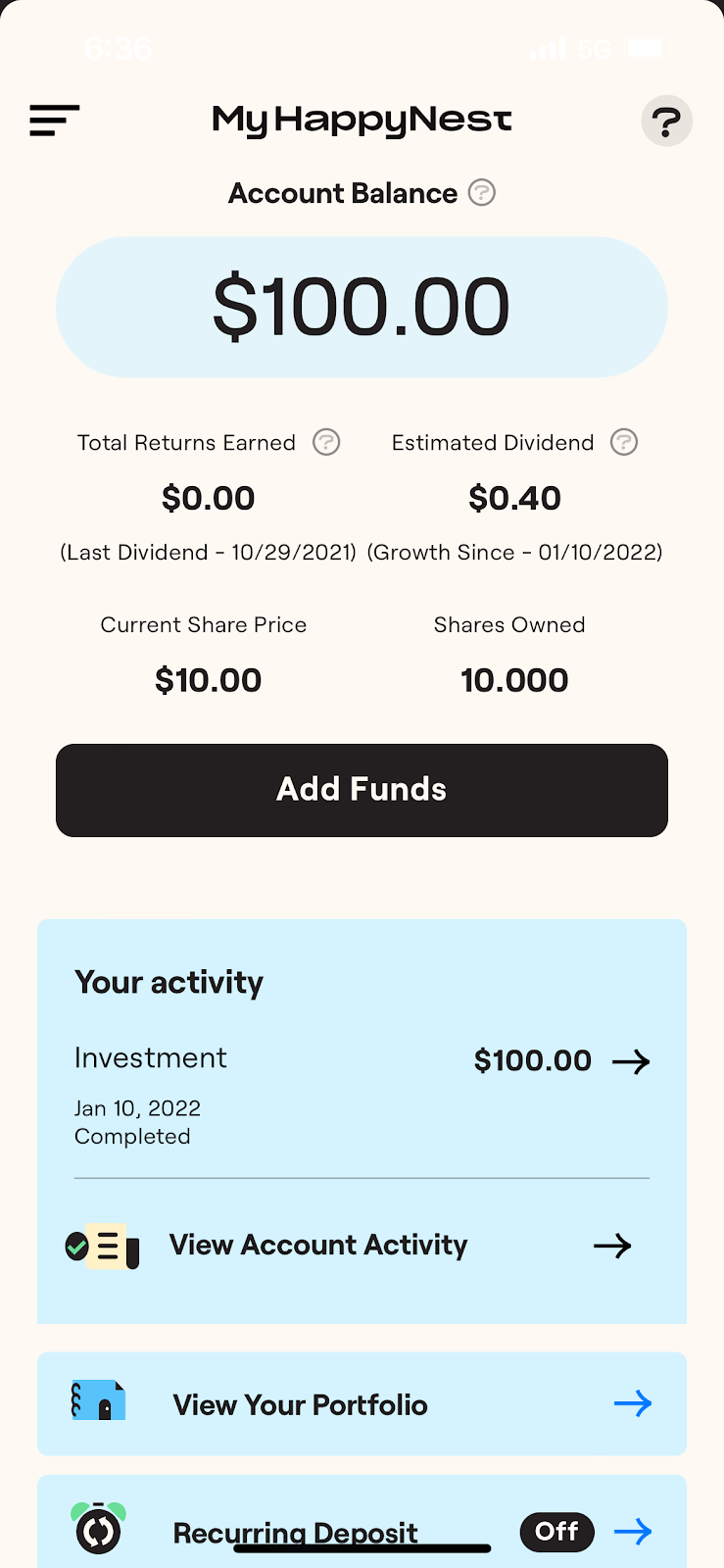

I signed up for HappyNest and made a small investment of $100 to see how the platform works.

Overall, I was a little disappointed in the value proposition that HappyNest offers to investors.

With a minimum investment of just $10, HappyNest is clearly targeting investors who are relatively new to the real estate market.

However, I saw a few reasons to think twice about this opportunity.

First, HappyNest has relatively low liquidity, with a minimum six-month holding period and penalties for all withdrawals made before the end of three years.

The other main issue is that HappyNest doesn’t offset that liquidity issue with strong targets.

In fact, there is no explicit target return listed on the site. The closest thing is a note that real estate can lead to a “return of up to 6% over time.”

HappyNest has generated returns well above 6% at some points. However, past performance is never a guarantee of future results.

Today, I’ll go over my experience with HappyNest and explain some of the best and worst aspects of the platform.

HappyNest At a Glance

| Minimum Investment | $10 |

| Annual Fees | None |

| Target Returns | None listed |

| Accreditation Required | No |

| Lock-Up Period | Minimum of six months; withdrawals made between six months and three years are subject to a small penalty |

| Property Types | Commercial, retail space |

| Project Types | Property management |

| Regions Invested In | United States |

| Tax Structure | REIT |

| Tax Document Provided | 1099-DIV |

| Dividend Reinvestment | Yes |

| 1031 Exchange-Eligible | No |

| Mobile App | Yes, mobile only |

How Does HappyNest Work?

HappyNest issues shares to its investors that represent the combined value of its properties.

Those properties are leased out to tenants who give HappyNest income in the form of rent.

By law, HappyNest and other REITs are required to pay out at least 90% of their annual income.

After a holding period of at least six months, investors will have the opportunity to request a share repurchase from HappyNest.

Investors receive that income as a dividend, which can either be withdrawn or reinvested.

Dividends are usually paid out quarterly, and you can see the current estimated dividend on the main account page in the mobile app.

However, shares are not redeemable for their full value until three years from the initial investment.

Additionally, all share repurchase requests are subject to HappyNest approval.

Property Types and Locations

HappyNest currently owns three retail and industrial properties:

| Property | FedEx Freight | CVS | AutoZone |

|---|---|---|---|

| Location | Fremont, Indiana | Easthampton, Massachusetts | Brick Township, New Jersey |

| Purchase Price | $21,301,478 | $5,340,000 | $3,214,285 |

| Annual Rent | $1,224,835 | $314,089 | $225,000 |

| Remaining Lease | 11+ years | 12+ years | 8 years |

| Planned Rent Increases | None | ~4% every five years | 5% every five years |

Based on information from its website, HappyNest doesn’t appear to be involved in building, renovating, or otherwise developing the properties they invest in.

Instead, HappyNest prioritizes investments that provide stable cash flow and are unlikely to require any major renovations.

Nothing is guaranteed in real estate, but since each property is already secured by a long-term lease from a major corporation, you should be able to rely on consistent cash yields.

This approach may help to reduce risk, but it could limit upside compared to investments that add value through renovations or development.

Since HappyNest isn’t making any major changes to its properties, I would expect their appreciation to roughly track the values of similar properties in the same regions.

If you’re looking for real estate opportunities with the highest potential returns, I would recommend looking at another platform instead of HappyNest.

Target Returns

HappyNest doesn’t list any desired returns on its website, so it doesn’t appear to have a specific target.

However, its website mentions that investing in real estate “offers a return of up to 6% over time.”

That isn’t very promising, especially considering that HappyNest doesn’t offer much diversification with a current total of just three properties.

As you’ll see below, HappyNest also comes with a significant commitment of at least six months.

Keep in mind that Fundrise’s 6% figure appears to refer to institutional real estate opportunities such as REITs.

Other types of real estate investments —for example, buying your own rental property — could offer significantly more upside.

At the same time, investments with higher potential returns will most likely come with a greater risk or require more effort on your part.

Alternative investments such as the S&P 500 and publicly traded REITs may offer a more attractive combination of diversification, liquidity, and upside compared to HappyNest.

If you invested $100 into the S&P 500 at the beginning of March 2017, you would have had $183.32 at the beginning of March 2022.

That works out to an annualized return of 12.89% —more than double the 6% figure mentioned on the HappyNest website.

The S&P 500 offers built-in diversification with exposure to 500 different companies, and you can buy and sell shares whenever you want.

Of course, some of you may be considering HappyNest as a way to get into real estate and diversify away from conventional index funds.

In that case, you might be more interested in how HappyNest compares to alternative real estate investments.

The table below shows the overall gains and annualized returns of five major publicly traded REITs: VNQ (Vanguard Real Estate ETF), IYR (iShares U.S. Real Estate ETF), SCHH (Schwab U.S. REIT ETF), NURE (Nuveen Short-Term REIT ETF), and SRET (SuperDividend REIT ETF).

| Fund | Final Value of $100 Investment | Annualized Return |

|---|---|---|

| S&P 500 | $183.32 | 12.89% |

| VNQ | $145.37 | 7.77% |

| IYR | $149.17 | 8.35% |

| SCHH | $126.37 | 4.79% |

| NURE | $163.99 | 10.40% |

| SRET | $88.08 | -2.51% |

Three of the five real estate funds returned more than 7% per year during that five-year period.

On the other hand, SRET’s poor performance brought the overall average down to about 5.8%.

6% per year seems like a reasonable estimate of real estate performance in general, but your returns could vary widely over time and between different real estate investments.

Minimum Investment

Users can get started with HappyNest with an investment of as little as $10.

HappyNest is entitled to charge an administrative fee of up to $1 per investor per month, which would make small investments basically pointless —you could lose a $10 investment in less than a year just through the monthly fee.

I have not been charged any administrative fees over six weeks, and it seems to be the same for other investors. That said, you should keep this possibility in mind and look out for any fees that might show up in your account.

As I mentioned earlier, the low minimum investment is a clear sign that HappyNest is trying to bring in novice investors.

There’s nothing wrong with HappyNest being your first foray into the real estate market, but you should fully understand the pros and cons of this investment — even if you only contribute the $10 minimum.

Investment Duration and Lock-Up Period

Unfortunately, you won’t be able to sell your HappyNest shares within six months of your initial investment.

After six months, you’ll have the opportunity to sell shares through the platform’s share repurchase program.

Shares are repurchased biannually, typically on March 31 and September 30.

However, all share repurchase requests are subject to HappyNest approval.

There’s no guarantee that you’ll be able to withdraw your funds, particularly if there’s a downturn and many investors are trying to pull out at the same time.

The other drawback of the share repurchase program is that you’ll lose a small percentage of the share value for any sales made before holding for three years.

The table below shows standard redemption prices in NAV (net average value) per share for sales at different intervals.

| Length of Investment | Share Redemption Value |

|---|---|

| Less than six months | No redemptions allowed |

| Six months to one year | 97% |

| One to two years | 98% |

| Two to three years | 99% |

| Over three years | 100% |

With these limitations, you should be extra careful to avoid investing unless you’re sure that you won’t need the money in the near future —at the very least, within the next six months.

Vetting and Review Process

There are a few clear trends in HappyNest’s early investments.

First, each one is occupied by a major consumer brand — FedEx, CVS, or AutoZone.

This reduces the risk of default or other issues with the lease, particularly compared to REITs that focus on multifamily properties.

Also, each of HappyNest’s tenants has agreed to a long-term lease.

In the case of the FedEx building, for example, FedEx is already bound more than ten years into the future.

If HappyNest continues to expand its holdings, I would expect the same trend to continue with conservative investments.

The long-term lease is a key part of HappyNest’s approach since it minimizes the risk of any cash flow disruptions.

Of course, HappyNest currently owns just three properties, so it’s difficult to say what their portfolio might look like in a few years.

Tax Implications

HappyNest makes distributions to investors in the form of dividends, which are taxed as conventional income.

You will receive a 1099-DIV form based on your dividend activity in January of each year after you’ve earned dividends through HappyNest.

At the end of your investment, any returns generated by your shares will be taxed (or deducted) as capital gains.

In general, assets are subject to short-term capital gains taxes when sold within one year, or long-term capital gains taxes when sold after a full year.

On top of paying less in penalties, you may also be able to save on capital gains taxes by holding your HappyNest shares for at least one year.

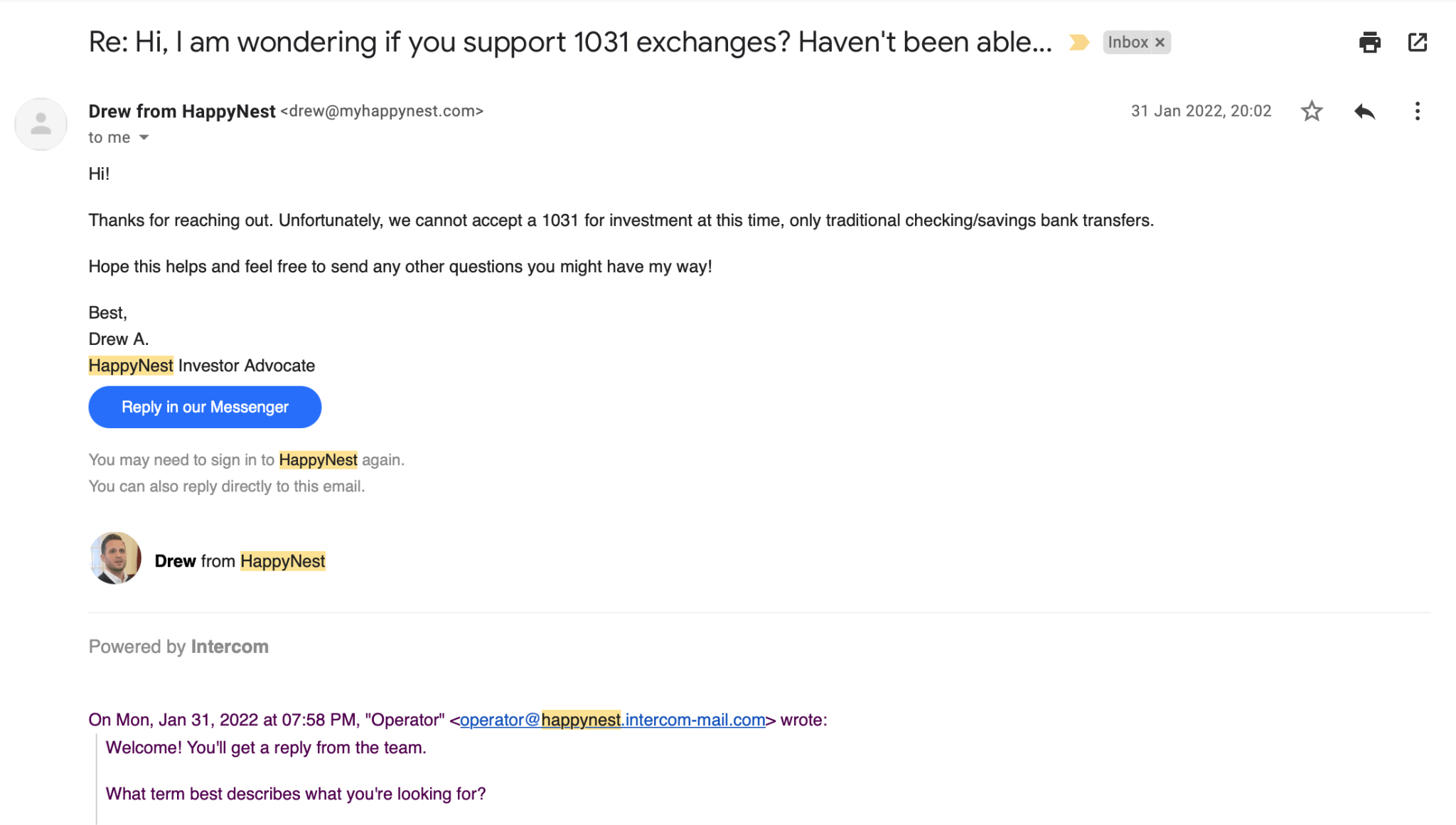

Customer Service

HappyNest is headquartered in New York City, so I was expecting a reply the next morning when I sent a message on a Monday night at roughly 8 PM EST.

Surprisingly, someone from their team got back to me in an incredible four minutes with a brief, clear response.

This was one of the best customer support experiences I’ve had with any investing platform.

Of course, it’s possible that other users may have more trouble getting in touch with the HappyNest team.

HappyNest Fees

HappyNest states that they do not charge any brokerage commissions or platform fees.

However, there are still a few charges that you should be aware of before making any investments.

Administrative Fee: HappyNest may charge an administrative fee to each investor. This fee could be as much as $1 per month and will be deducted from your linked bank account.

Organization and Offering Expenses: According to the HappyNest offering circular, HappyNest will pay its sponsor up to 3% of aggregate gross offering proceeds once 30,000 shares have been sold at $10 per share.

Asset Management Fee: HappyNest pays its advisor an asset management fee of 0.0417% of total invested value per month, which works out to one-half of one percent over the course of a full year.

Acquisition and Disposition Fees: HappyNest typically pays its advisor 3% of the contract price of each property that’s purchased or sold. However, HappyNest will not pay the full 3% to the advisor if that would take the total broker fees associated with a given property over 6%.

For example, if HappyNest is already paying 4% in broker fees on a particular sale, then they will only pay 2% to the advisor for a total of 6%. On the other hand, the advisor would receive the full 3% in a case where HappyNest was only paying 2% or 3% in other fees.

Property Management Fee: The HappyNest offering circular states that “properties are intended to be triple-net single tenant properties with limited property management responsibilities.”

In cases where the advisor or an affiliate provides property management, HappyNest will pay the advisor up to 1% of gross revenues from the properties being managed. They may also pay for some out-of-pocket expenses as well as “property-level expenses that [the advisor] pays or incurs on [HappyNest’s] behalf.”

Independent Director Compensation:

The HappyNest website prominently advertises that there are no “broker or platform fees.”

While that might be technically true, it doesn’t feel like the full truth when you compare it with HappyNest’s full fee structure.

As an investor, I don’t really care that there aren’t any “broker commissions” when HappyNest pays up to 6% in broker fees for acquisitions and dispositions.

In the same way, it’s hard to understand how there can be no “platform fees” associated with HappyNest.

Personally, if I’m paying 0.5% per year for asset management, I don’t see how that’s any different from a platform fee.

Given the selective wording, this seems like a pretty clear attempt to make inexperienced investors think “Wow, no broker commissions or platform fees!” without reading the fine print.

Is HappyNest Legit?

Every investment comes with some risk, but HappyNest is a totally legit opportunity.

They submitted an offering circular to the SEC in July of 2021. The terms of that offering appear somewhat ominous:

“Neither the SEC, the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved the common stock of the Company, determined if the Offering Circular is truthful or complete or passed on or endorsed the merits of the Offering.”

However, there’s nothing particularly unusual about this practice. In short, this just means that you need to do your own research to evaluate the platform’s upside and risks.

HappyNest is exempt from SEC registration under Regulation A, which applies to public offerings of up to $75 million in a 12-month period.

Even though it isn’t treated like a conventional stock or mutual fund, HappyNest is still subject to certain rules and regulations.

Naturally, it can still be penalized for fraudulent statements and other forms of misconduct.

To put it more plainly: There’s no reason to believe that they’ll run off with your money.

Furthermore, HappyNest is listed as a REIT on the SEC website, which also hosts all relevant documentation.

They publish two reports per year: one in April and another in September.

So while HappyNest probably won’t scam you out of your funds, it’s important to realize that this doesn’t necessarily make it the right investment opportunity for you; you have to weigh the pros and cons of the platform.

HappyNest Pros and Cons

HappyNest’s low minimum investment is a major advantage over many other real estate opportunities, making it easier for people to get involved in real estate investing regardless of their budget.

Pros

Pros

- $10 Minimum Investment: You only need $10 to get started with HappyNest.

- Availability: You don’t have to be an accredited investor to use HappyNest.

- Solid Mobile Reviews: The mobile app has an average user rating of 4.1 on Android and 4.2 on iOS.

Cons

Cons

- Long-Term Commitment: Withdrawals can be denied by HappyNest, and you will need to hold for at least three years in order to receive the full value of your shares.

- Limited Diversification: HappyNest currently owns three properties, which means that any one of them could have a dramatic impact on your returns.

- Potentially Low Returns: HappyNest doesn’t provide an explicit target return, but the note that real estate offers gains of “up to 6%” isn’t promising.

Alternatives to HappyNest

| HappyNest | DiversyFund | Arrived Homes | Fundrise | |

|---|---|---|---|---|

| Property Types |

|

|

|

|

| Property Locations |

|

|

|

|

| Target Returns |

|

|

|

|

| Minimum Investment |

|

|

|

|

| Minimum Duration |

|

|

|

|

| Accredited Investors Only? |

|

|

|

|

Is HappyNest Worth It?

Even if you aren’t financially prepared to buy property on your own, you may still want to add real estate to your investment portfolio.

HappyNest appeals to many investors due to its low minimums, but there are also a few good reasons to consider other platforms.

First, HappyNest only includes a total of three properties, which means that investors can only access limited diversification.

If you invest in 100 different properties with roughly the same value, then no individual investment can impact your portfolio more than 1%. With HappyNest’s set of three properties, each one makes up 33% of your total return.

Alternative real estate investments like DiversyFund provide exposure to a wider range of properties.

Investors may also prefer to stay away from HappyNest due to its limited liquidity.

While HappyNest investments must be held for a minimum of six months, publicly traded REITs can be bought and sold at any time.

The downside of this liquidity is that publicly traded REITs tend to fluctuate more dramatically since the price can change at any time based on investor sentiments that may not be related to the value of the underlying real estate.

With that in mind, HappyNest may be worth it for investors who want to put a small amount in real estate, who are willing to hold for at least six months, and who believe in the three properties that are currently included in the fund.

Who HappyNest Is Best For

HappyNest is best for people who want to invest in real estate and are willing to hold for at least three years.

Furthermore, HappyNest could act as a hedge for renters.

Without a real estate investment of your own, growth in the real estate market will only mean an increase in rent.

On the other hand, renters who hold HappyNest shares will also have something to gain if real estate gains value.

Even if you’re a homeowner, you may be interested in diversifying so that you have more than just residential real estate.

HappyNest could be an easy way to get involved in commercial real estate while also investing in properties in different locations.

Who HappyNest Is Not For

HappyNest is not for people who want a short-term, liquid investment.

If you don’t have substantial savings or an emergency fund to fall back on, you should think twice before putting too much money into HappyNest or any other long-term investment.

Remember that your financial security should take priority over more speculative opportunities. You should only invest funds that you’re comfortable committing to HappyNest for at least three years.

How to Use HappyNest (Step-by-Step)

- Download the HappyNest app (available on iOS and Android).

- Create an account with your email and password, or sign up through Google, Twitter, or Apple.

- Link your bank account to HappyNest.

- Add funds to your HappyNest account.

Final Thoughts

Real estate investing used to be relatively inaccessible to everyday investors, but HappyNest and other similar platforms are reducing minimum investments and removing other common barriers.

Investing with HappyNest comes with some notable drawbacks.

Your shares will be tied up for six months, and at least three years if you want to redeem them for their full value.

Furthermore, with only three total properties, your investment won’t be exposed to the same diversification as you could get with a more conventional REIT.

On the other hand, HappyNest’s focus on properties with long-term leases from major businesses may give it a more favorable risk profile compared to other kinds of REITs — for example, those that are mostly invested in multifamily properties, or that expect to generate much of their returns from development or renovations.

Frequently Asked Questions

- Do I have to be an accredited investor to invest in HappyNest?

- How do I withdraw from HappyNest?

- Who owns HappyNest?

Author:

Logan is a practicing CPA and founder of Choice Tax Relief and of course Money Done Right. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money. Learn more about Logan.